HSIE Institutional Report: IRM Energy Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 05:53 PM IST

Industrial PNG Volume Continues to Decline

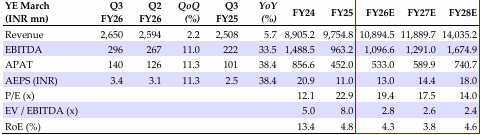

Our BUY recommendation on IRM Energy (IRM) with a TP of INR 402/sh is premised on (1) a ~13% CAGR volume growth over FY26-28E and (2) per unit margin expansion in the long term. IRM’s Q3FY26 EBITDA at INR 296mn (+33.5% YoY, +11.0% QoQ) and consolidated PAT at INR 140mn (+38.4%YoY, +11.3% QoQ) came in below our estimate due to lower-than-expected Industrial PNG volumes. Total volume stood at 0.61mmscmd (+4.8% YoY, +2.6% QoQ)

IRM Energy Volume

IRM’s volume at 0.61mmscmd (+4.8% YoY, +2.6% QoQ) came below our estimate. The miss was due to weaker-than-expected Industrial PNG volumes. CNG volume stood at 0.37mmscmd (+20.6% YoY +6.8% QoQ). Domestic PNG segment volume was 0.03mmscmd (+14.0% YoY, +4.1% QoQ), and industrial and commercial segment volume was 0.21mmscmd (-14.1% YoY, -4.3% QoQ). We expect IRM to maintain its CGD network expansion, which should support our projected ~13% CAGR volume growth from FY26 28E. Our volume estimates for FY26/27/28E stand at 0.60/0.67/0.76msmcmd.

Higher Gas Cost Impacts Per Unit Margins

Blended realization at INR 47.3/scm was up 0.9% YoY and down 0.4% sequentially. Raw material cost stood at INR 35.1/scm (-2.3% YoY, -0.9% QoQ), resulting in gross spreads of INR 12.2/scm (+11.5% YoY, +1.0% QoQ). Other expenses came in at INR 6.9/scm (+1.8% YoY, -3.9% QoQ). EBITDA per unit at INR 5.3/scm (+27.4%YoY, +8.2%QoQ) was below our estimate due to higher-than-expected opex. We factor in EBITDA per unit assumption of INR 5.0/5.3/6.0 per scm for FY26/27/28E.

Other Highlights

(1) CNG – Volume growth was led by the Banaskantha and Diu, Gir, & Somnath GAs. IRM added 11 CNG stations during the quarter, taking the total count to 127. Management remains optimistic of this segment, posting double-digit growth in FY27E, owing to strong CNG vehicle adoption. For 9MFY26, CNG gas sourcing stood as follows – 41/38.4/7.5/13.1% from APM/HPHT/NWG/Spot and long-term contracts. (2) PNG – Demand from the Industrial customers in Fatehgarh Sahib GA continued to remain under pressure as prices of alternative fuels remained lower than that of PNG. This resulted in PNG volume in FS GA declining YoY in 9MFY26. IRM believes that the hearing on the NGT order being passed in favor of Natural Gas adoption will lead to a demand revival in this GA. Guidance – Volume growth for FY27 will be in the range of 12-15% and EBITDA per unit will be in the range of INR 5.25-5.5/scm.

DCF-Based Valuation

We cut our FY26/27E EPS estimates by 9.5/15.0% as we factor in the sub-par demand from the industrial customers, dragging down the total volume growth. Our target price of INR 402/sh is based on Mar-27E free cash flow (WACC 13.7%, terminal growth rate 2%). The stock is currently trading at 17.5x Mar-27E EPS.

IRM Energy Consolidated Financial Summary

Changes in Estimates

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.