HDFC Securities Institutional Research Report: JK Lakshmi Cement Feb, 05 2026

Authored By Prime Research | Last Modified: Feb 5, 2026 02:21 PM IST

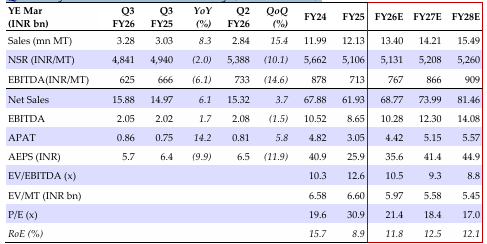

Healthy Volume Growth; Dismal Margin Performance

We retain BUY on JK Lakshmi (JKLC), with a revised TP of INR 930/share (10x FY28E consolidated EBITDA). In Q3FY26, while JKLC maintained healthy volume growth momentum (+8/15% YoY/QoQ), margin slumped INR 107/MT QoQ to INR 625/MT on a sharp fall in non-trade realization. We estimate JKLC will deliver 8/18% consolidated volume/EBITDA CAGRs. The ongoing expansion in the eastern region and UP would get commissioned in FY28E. The company expects capex run-rate to accelerate Q4FY26E onwards. Given the slower expansion, we expect its net debt to EBITDA to remain comfortable and peak out at 2x in FY28E.

Q3FY26 Performance

JKLC delivered healthy volume growth of 8/15% YoY/QoQ. This was led by strong ramp-up of the Surat SGU which also led to increase in non-trade sales: 51% vs 47/42% QoQ/YoY. The share of premium cement sales was flattish QoQ at 26%. Higher non-trade sales in Gujarat and Mumbai markets, as well as sharper correction in non-trade prices in Q3 led to JKLC reporting cement/blended NSR decline of 9/10% QoQ. Unit opex also fell 9% QoQ on lower freight cost (lead distance reduction and higher ex-factory sales), lower employee costs (head count rationalization to boost productivity) and lower input cost (unexplained). Unit EBITDA slumped INR 107/QoQ to INR 625/MT. JKLC spent ~INR 1/3.5bn in capex in Q3/ 9MFY26.

Con Call KTAs and Outlook

The company remains upbeat on cement demand in Q4 and expects it to grow at 10%+ while also expecting its growth to be in-line with industry’s growth. While its capex outgo was low in Q3, JKLC guided that capex run rate will accelerate to ~INR 3.5/4bn in Q4FY26 and INR16-17bn in FY27. It reiterated that its east expansion is on track and will be commissioned in phases by Mar-26E/Mar-27E. Phase-2 expansion of the railway siding in Durg is now expected by Mar-28. Factoring in weak pricing and slower expected pace of east expansion, we have trimmed EBITDA estimates for FY26/27/28E by 6/11/11% respectively.

Quarterly/Annual Financial Summary (Consolidated)

Source: HSIE Research (HSIE Results Daily – 05 Feb 26 – HSIE-202602050642042086559.pdf)

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.