HSIE Institutional Report: Kansai Nerolac Feb, 05 2026

Authored By Prime Research | Last Modified: Feb 5, 2026 02:19 PM IST

Industrial Cushions Growth; Margins Disappoint

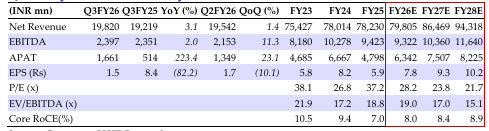

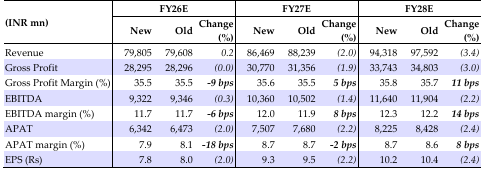

Kansai Nerolac’s (KNPL) standalone revenue grew 3.5% YoY to INR19bn (in line). While a subdued environment and a shorter festive season led to a low-single-digit volume/value decline in decorative, with the topline buoyed by double-digit value growth in the industrial segment, driven specifically by a GST-led demand surge in automotive. GM expanded by 24bps to 35.5% (HSIE: 36.2%) as benign raw material costs were partially impacted by higher industrial mix. However, EBITDAM contracted by 44bps YoY to 13% (HSIE: 13.4%) due to higher manpower investments. Near-term EBITDAM guidance of 13-14% stays. We have cut our FY27/28 EPS estimates by ~2% each and maintain REDUCE with a DCF-based TP of INR235/sh (implying 23x Mar-28 P/E).

Kansai Nerolac Q3FY26 Highlights

Standalone revenue grew 3.5% YoY to INR 19bn in Q3 (in line), while consolidated revenue grew 3.1% YoY to INR 19.8bn. Decorative segment posted low-single-digit value decline, while industrial reported double digit value growth. The company added over 3.5k dealers in 9MFY25. In decorative, demand was tempered by subdued environment and a shorter festive season; however, internal initiatives led to double-digit growth in project business, CC, waterproofing, and premium wood finishes. Paint+ category now contributes >10% to decorative business, while services contribute >5%. In industrial, auto segment reported strong growth in Q3, fueled by GST rate cut which spurred demand across various OEM categories. In performance coatings, liquid coatings witnessed strong demand in GI while demand momentum remained stable in powder coating driven by auto ancillary. Auto refinish demand remains stable. Bangladesh print remained weak, while Nepal continued to perform well. Standalone GM expanded by 24bps to 35.5% (HSIE: 36.2%), driven by benign raw material prices, partially impacted by higher industrial mix. However, EBITDAM contracted by 44bps YoY to 13% (HSIE: 13.4%) due to higher manpower cost. Management maintains EBITDAM guidance of 13-14% in the short term. EBITDA remained flat YoY at INR2.47bn (HSIE: INR2.54bn), while APAT declined 3.7% YoY to ~INR1.6bn (HSIE: INR 1.73bn).

Outlook

While the recovery timeline for decorative paints remains unclear, KNPL’s stronghold in industrials continues to cushion the overall sales impact. We have cut our FY27/28 EPS estimates by ~2% each and maintain REDUCE rating with a DCF-based TP of INR235/sh (implying 23x Mar-28 P/E).

Kansai Nerolac Quarterly Financial Summary (Consolidated)

Change in Estimates

Source: HSIE Research (HSIE Results Daily – 05 Feb 26 – HSIE-202602050642042086559.pdf)

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.