HSIE Institutional Report: Lemon Tree Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 11:33 AM IST

Soft Performance Continues in a Seasonally Strong Q3

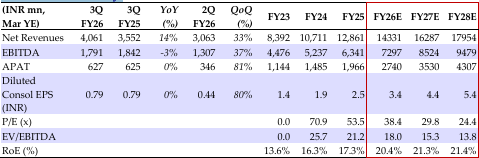

Lemon Tree Hotels (LTH) recorded a lacklustre Q3FY26 performance, reflected in 9% YoY RevPAR growth, led by 11% YoY ARR growth but 82 bps YoY decline in occupancy (73.4% in Q3FY26). This clearly shows reluctance of key markets to accept ARR increase. Further analysis indicates that in the markets of Gurugram, Hyderabad, and Bengaluru, raising ARR resulted in a sharp decline in occupancies, reflecting resistance to further ARR increase. On the other hand, Delhi, Mumbai, and Pune easily accommodated ARR increase reflected in increased occupancies, thus proving market depth and demand strength. Revenue grew 15% YoY to INR4.1bn, reflecting soft RevPAR growth and unchanged owned room inventory (total owned rooms: 5759). EBITDA margin for the quarter declined to 44% (-820 bps YoY), led by renovation, GST, and labor code impact to the tune of INR 313mn. The number of managed rooms grew impressively by 32% YoY to 6,013; however; management fee income (INR 482 mn) rose by only 10% YoY as several newly opened hotels are yet to stabilize and ramp up their operations. Management expects to be debt-free post the listing of Fleur Hotels. All asset heavy operations including under construction Aurika Shimla and Shillong hotels will be under Fleur hotels post restructuring. We believe the key growth drivers for LTH include RevPAR growth, led by occupancy and ARR growth in the owned hotels portfolio (Mumbai, Pune, and Delhi) and rising fee income, driven by mid-teen growth in number of managed rooms. Additionally, EBITDA margin expansion levers are a reduction in renovation expenses. Driven by a favorable supply demand mismatch in key locations and expected improvement in operational parameters, we believe revenue and EBITDA will grow at ~11% and ~15% over FY25-FY28E. We have cut EBITDA estimates for FY26 and FY27 by ~2-3% but retain estimates for FY28. We continue with a BUY rating for a TP of INR 187 (17x FY28 EV/EBITDA).

Lemon Tree Q3FY26 Highlights (Consolidated)

ARR for the quarter was INR 7,487 (+11% YoY) along with occupancy of 73.4% (-82 bps YoY), resulting in a RevPAR growth of 9% to INR 5,494. Available hotel rooms grew by a 14% to 11,772, led by 32% YoY growth in managed rooms to 6,013, as the number of owned rooms remained unchanged. Revenue grew 15% YoY to INR4.1bn, in line with estimates. EBITDA declined by 3% YoY to INR 1.8bn. PAT growth was stagnant YoY at INR 627mn, missing the estimates by 21.6%.

Brand Wise Performance in Q3FY26

Aurika’s occupancy increased to 74% (+266 bps YoY), while ARR rose by 5% YoY to INR 10,984. This led to a 9% growth in RevPAR to INR 8,109 for the flagship brand. Lemon Tree Premier has reached near-peak occupancy, maintaining it at ~81% (-35 bps YoY), and increased ARR by 8% YoY to INR 8,506. Lemon Tree Hotel’s ARR grew by 13% YoY to INR 7,081, maintaining an occupancy of 73% (-353 bps YoY), resulting in a RevPAR growth of 8%. Red Fox and Keys had an average ARR of INR5,016 (+17%YoY) and INR4,443 (+19% YoY) at occupancy rates of 70% (-470 bps YoY) and 62% (+317 bps YoY). Keys has a lower occupancy due to ongoing renovation. Overall, occupancy and ARR for the entire portfolio could improve steadily once renovation is over in FY27.

Outlook

LTH is planning a strong expansion by building a portfolio of 21,942 rooms across 259 hotels, up from 11,772 at present (owned and leased: 5,759 rooms across 41 hotels). 93% of the pipeline could be managed/franchised, reiterating an asset-light growth strategy. Management estimates operationalize ~3,000 rooms in FY26 (opened in 9M FY26: 1,480 rooms) and ~2,000 in FY27, which we believe has a downside risk. Hence, we build ~2,000 and ~1,300 room additions for FY26 and FY27. We expect increase in ARR for Aurika, Mumbai. We also expect stable occupancy and mid-single digit growth in ARR for the overall portfolio to be driven by demand tailwinds and support a ~15% EBITDA CAGR over FY25-FY28E.

Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.