HSIE Institutional Report: Life Insurance Corporation of India Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 09:36 AM IST

Strong Growth and Improving Product Mix

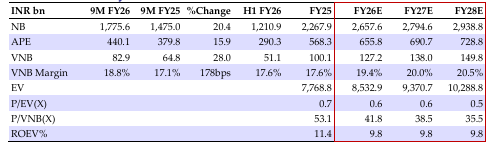

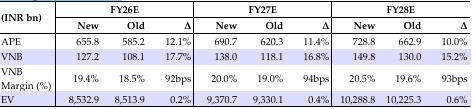

Life Insurance Corporation of India (LICI) printed a beat on APE growth (+16% YoY), led by a strong rebound in Individual segment (9M: +12%YoY, H1: 5%YoY). VNB grew much stronger by +28% YoY as VNB margins clocked in at 18.8% (+170bps YoY), ahead of expectations, driven by improved product mix and retail growth rebound. Traditionally focused on the mass customer segment, LICI has engineered a shift in its product strategy toward a higher sum-assured, non-PAR policies over the past couple of years (FY25: 28% of new business). LICI derives its moats from a large agency network while undergoing a strategic shift in its individual product proposition to align itself to the new surrender guidelines (implemented from Oct-24). We revise our APE/VoNB CAGR to 9/14% over FY25-FY28E and expect VNB margin expansion to continue on the back of improvement in product profiles to 20.5% by FY28E. We revise RoEV estimates to 9.8% during FY25-28E, primarily on account of the unwinding and VNB and maintain our ADD rating and with a revised TP of INR1,090 (0.7x Sep-27 EV).

Growth Rebound in the Individual Business

In Q3, LICI witnessed strong growth in individual business segment of 61% (H1: -5%), led by growth in number of policies (77% YoY). Growth in Q3 was underpinned by strong performance across segments’ NPAR savings >100%. We believe with reset in base, LICI is set to grow faster than the industry for next couple of quarters.

Revamped Product Construct

LICI has revised its product construct through higher policy premium (PAR), lower IRR (NPAR), lower commission for non club agents, and introduction of club-wise commission structure for agents. LICI has shifted its product strategy toward higher sum-assured, non-PAR, policies over the past couple of years (9MFY26: 36.5%; FY25: 28% of new APE). In Q3, we surprisingly witnessed growth of 49% in PAR, which had not grown, given changes made in product constructs.

Improving RoEV to Drive Re-Rating

We believe LICI has been able to execute multiple changes to its historic business efficiently. LICI lowered the share of PAR in product mix over the last couple of years and reduced its dependence on the agency channel (9MFY26:91.7%, FY25:96%). We argue increase in the dividend payout ratio would be a key for its potential re-rating, which would improve the RoEV to low teens.

Life Insurance Corporation of India Financial Summary

Change in Estimates

Source: HSIE Research (HSIE Results Daily – 06 Feb 26 – HSIE-202602060713371815208.pdf)

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.