HSIE Institutional Report: Mahanagar Gas Feb, 10 2026

Authored By Prime Research | Last Modified: Feb 10, 2026 12:42 PM IST

Lower Gas Costs Lift Margins

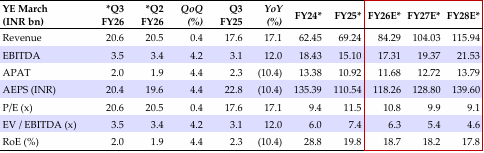

Our BUY recommendation on Mahanagar Gas (MGL) with a target price of INR 1,880 is premised on a strong 10% volume CAGR over FY25-27E, led by accelerated addition of retail outlets, customer additions in the industrial segment, and continued firm CNG vehicle registration. The Q3FY26 consolidated EBITDA came in at INR 3.52bn (+8.4% YoY, +4.2% QoQ) and consolidated PAT was at INR 2.01bn (-9.1% YoY, +5.2% QoQ). The sequential improvement in profitability owed to lower raw material cost, which was partially offset by higher operating expense.

Standalone Volume Growth at 3.4%YoY

MGL’s quarterly standalone volume grew by 3.4% YoY to 4.62mmscmd. CNG/PNG volume came in at 3.28/1.34mmscmd (+0.2/11.9% YoY). Industrial and commercial segment and DPNG volume stood at 0.74/0.60mmscmd (+13.8/9.5% YoY).

Margins Improve

Standalone per unit gross margin improved to INR 15.1/scm (+19.5% YoY, +2.3% QoQ). Per unit opex stood at INR 6.8/scm (+25.2% YoY, +0.7% QoQ) and standalone EBITDA increased to INR 8.3/scm (+15.1% YoY, +3.6% QoQ). Better gas sourcing mix has resulted in a fall in per unit raw material cost in the quarter.

Conference Call Takeaways

(1) CNG – Mumbai’s volume growth remained muted at ~2% YoY due to land scarcity for new stations and BEST bus felt size reducing from 3,000 to a few hundreds. In addition, pipeline disruption during the quarter caused a volume loss of 1%. 35-40% of CNG revenue comes from private cars and taxis, 35-40% from three-wheelers, ~8% from state transport undertakings and balance from commercial goods vehicles and private buses. MGL undertook a price hike of INR 1.5/kg in order to maintain margins amidst rising Henry Hub prices. (2) PNG – Industrial and commercial PNG segment volume was impacted in the quarter due to the pipeline disruption. While realization from the I&C PNG segment was lower in Q3FY26 due to lower Brent crude prices, management expects realization to improve as Brent crude prices inch upwards.(3) Gas sourcing – ~39% of the total demand was met through APM gas, 6% through New Well Gas, ~ 30% from HH linked contracts and the remining demand of ~25% was met through Brent-linked contracts. MGL replaced some amount of HH linked contracts with HPHT and spot gas in Q3 in order to manage raw material cost. (4) MGL aims to report a double-digit volume growth in Q4 and maintain this growth through FY27. The company has maintained its long-term margin guidance range of INR 8-9/scm.

DCF-Based Valuation

We maintain BUY with a target price of INR 1,880/sh, based on Mar-27E free cash flow (WACC 10.5%, terminal growth rate 2%). The stock is currently trading at 9.9x Mar-27E EPS.

Mahanagar Gas Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 10 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.