HSIE Institutional Report: Mahindra & Mahindra Feb, 12 2026

Authored By Prime Research | Last Modified: Feb 12, 2026 11:51 AM IST

Good Outlook For Autos, Though No Guidance For Tractors

Mahindra & Mahindra’s Q3FY26 standalone EBITDA margin at 14.7% missed our estimate by 28bps, while it was in line with Bloomberg consensus estimate. While autos look well poised on continuing demand momentum and up trading trends, tractor outlook remains uncertain due to a high base and considering early forecasts of El Nino in India during the latter half of monsoon in 2026. Additionally, we expect an increase in ePV contract manufacturing and recording of PLI benefits in subsidiaries, to impact the standalone auto business margins over the near to medium term, as the company pushes to increase its EV mix, in light of the upcoming CAFÉ norms. Though this should improve the financials of the EV subsidiaries. We value the company on a SOTP basis, with the core business valued at 21x Dec-27 EPS for a target price of INR4,348 and maintain an ADD rating.

Mahindra & Mahindra Quarterly Performance

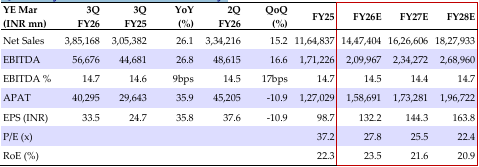

Standalone revenue at INR 385.2bn grew 26.1% YoY and 15.2% QoQ, led mainly by volume growth. Auto division’s EBIT margin at 9.5% improved 32bps QoQ (HSIE est. 9.4%), while the core auto (ex-BEV) margin stood at 10.4% (up 10bps QoQ). Farm division’s EBIT margin at 20.2% continued to impress (core tractor margin at 21.2%), ahead of our estimate of 20.1%, led by better operating leverage. Farm machinery revenue grew 45% YoY to INR 3.6bn.

Upcoming Launches and Capacity

Management highlighted upcoming launches for CY26: 3 ICE SUVs (one is 7XO while two more model refreshes are awaited), 2 BEVs (both are already launched), and 2 LCVs (still pending). On the capacity expansion plan, it commented that CY26 will entail debottlenecking at the Nashik plant for the 3XO and Bolero models and at the Chakan plant for the Scorpio N model. From this, it aims to add capacity of 3k units per month by July, along with another 3k planned for BEV. In CY27, the new capacity at Chakan will cater to the NU_IQ models (Vision S or Vision T, both to be launched in CY27). In CY28, the greenfield at Nagpur will further aid capacity, primarily for the NU_IQ models.

Farm Segment

Management held back from giving guidance for FY27, though highlighted that in case of below normal monsoon, healthy reservoir levels should support farming activity. While it lost some market share in Q3 due to lower supply of the Swaraj brand, it has seen a recovery in Jan.

Management Commentary Takeaways

(1) It expects the demand momentum for LCV to continue for some time, as profit improvement for the operator post the GST rate cut is 4-5%. (2) The 7XO has a strong order pipeline with a big skew towards the top end variants, despite of very good lower variant products. (3) It highlighted up-trading across models and variants in SUVs post the GST rate cut. 4) It mentioned that higher raw material costs may impact in the coming quarters, though it took a 1% price hike in Jan.

Quarterly/Annual Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 12 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.