HSIE Institutional Report: Max Financial Services Feb, 13 2026

Authored By Prime Research | Last Modified: Feb 13, 2026 05:19 PM IST

Strong and Profitable Growth

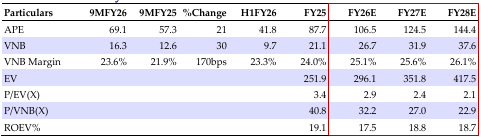

Axis Max Life Insurance (AMLI) reported YoY APE/VNB growth of +21/30% for 9MFY26. VNB margin expanded to 23.6% (+170bps YoY), clocking in ahead of our estimates, despite a one-time impact of wage cost (INR0.6bn) and GST ITC disallowance (INR3bn). Contrary to the earlier guidance of impact of 300 350bps on VNB margin due to loss of GST ITC, it was negated to a large extant with mix shift toward non-ULIP segments (9MFY26: 62.7%; H1FY25: 54.6%) and distributor costs rationalization. AMLI sustained strong growth (+57% YoY) in the health and protection business amid its continued focus on rider attachment (attachment rate at ~37%). We expect that, with GST ITC unavailability, VNB margins for FY26E are likely to keep VNB margins under check despite the favourable shift in product mix. We build in 18/21/18% CAGR in the APE/VNB/operating RoEV for FY25-28E; maintain ADD with a TP of INR1,750 (implied 2.2x Sep-27E EV prior to 10% hold-co discount, 6% implied discount to SBILIFE).

Likely to Become Third Largest Amongst the Private Player

IRNB growth (x1.5 private players) continued to outpace private life insurers for 9MFY26, led by the non-AXSB banca partnerships (+41% YoY), while the proprietary offline channel grew +29%. The AXISB channel continued to show signs of growth fatigue (+8% YoY), though management highlighted that growth in Q4 is likely to rebound in AXISB on a softer base. We believe given the current IRNB growth trends, AMLI will surpass TATAAIA in FY27E to become the third-largest life insurer amongst the private life insurers.

Retail Protection Growth Further Strengthens

AMLI continued to increase its mix of term insurance within individual APE to 13.7% (9MFY25: 10.5%), with its relentless focus on pure protection and rider attachments. As the growth in protection business (9MFY26:52%, Q3:>90%) in the proprietary channels was significant, we expect the share of term insurance to average mid-teens over FY26E-FY28E.Amongst the listed players, AMLI has the highest share of the term business in the individual APE.

Sustaining Current Growth Levels Remains Key to Current Valuation Levels

Management aspires for IRNB growth to be +500bps of the industry, we expect current valuations to factor in nearly a high-teen growth in topline which is important for sustaining the current valuation multiple and hence offers a limited upside.

Financial Summary

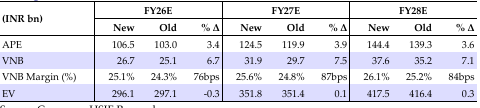

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 13 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.