HSIE Institutional Report: Navin Fluorine International Feb, 10 2026

Authored By Prime Research | Last Modified: Feb 10, 2026 11:52 AM IST

Speciality Chemical Business Drives Revenue

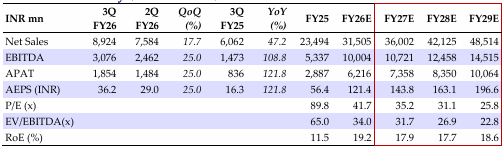

Navin Fluorine International’s (NFIL) strategy is to deepen wallet share within its existing customer base by leveraging its established marketing network, broadening its product portfolio, and building on long-standing client relationships, which will help drive growth across all business verticals. The CDMO business remains focused on select marquee global customers, with an emphasis on scaling revenues from commercial projects and late-stage molecules to secure more stable revenue streams, supported by its sustained engagement with leading innovator pharma clients. Concise to that, NFIL has commissioned cGMP 4 phase 1 with a capex of INR 1.6bn. HPP business and speciality chemical business will be led by deepening relations with existing customers and ramp-up in facilities. Changing global supply chain dynamics and incremental capex in the refgas business will help in ramping up the HPP business. EBITDA is expected to improve from INR 5.3bn in FY25 to INR 14.51bn in FY29 while EBITDA margins are expected to improve by 720bps to 29.9%, supported by inflection in the CDMO business and improved realization in refgas business with support of backward integration in AHP. Thus, we retain a BUY on NFIL with a target price of INR 7,260. EBITDA and APAT was 10% and 7.6% above our estimates.

Financial Performance

In Q3FY26, revenue increased by +47.2/+17.7% YoY/QoQ% to INR 8,924mn. EBITDA margin improved by +1,017/+201 bps YoY/QoQ bps to 34.5%, owing to improved realization in both HPP and CDMO business and operating leverage in spec chem business. EBITDA came in at INR 3,076mn (+109/+25% YoY/QoQ.

Specialty Chemical (40% of revenue)

Revenue in the quarter changed by +60.2/+60.9% YoY/QoQ to INR 3,540mn. Growth in revenue was majorly led by improved utilization of Nectar plant. Management expects better offtake in volume over FY27 due to improved outlook and strong visibility.

HPP Business (46% of revenue)

Revenue in the quarter changed by +34.6% YoY while majorly remaining in line with Q2 to INR 4,120mn. Growth was led by improved realization and volume in the quarter. R32 plant is almost running at full utilization. NFIL commissioned AHF plant in Q3FY26, which will be majorly consumed internally.

CDMO Business (14% of revenue)

Revenue changed by +60.7/-5.2% YoY/QoQ% to INR 1,240mn. NFIL completed validation and commercial supplies started at cGMP4 phase 1. Another EU major has provided scale-up orders in Q4FY26. There is balance of 50/50% in late stage and early stage molecules in pipeline. Management expects readouts for more than one molecule in FY27, which can move toward commercialization.

Change in Estimates

We change our FY26/FY27/FY28E EPS estimates by +16.8/+2.5/+1.8% to INR 121.4/143.8/163.1x due to better-than-expected performance in Q3.

Financial Summary (Consolidated)

Change in Estimates (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 10 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.