HSIE Institutional Report: Neogen Chemicals Feb, 13 2026

Authored By Prime Research | Published at: Feb 13, 2026 05:06 PM IST

Projects on Track

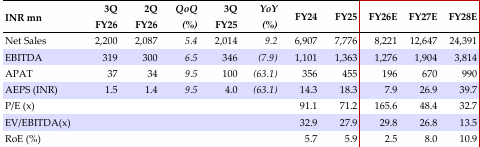

Our BUY recommendation on Neogen Chemicals (NCL) with a target price of INR 2,761/share is premised on (1) entry into the new-age electrolyte manufacturing business; (2) increasing contribution of the high-margin CSM business to revenue; and (3) volume-driven growth in legacy business. NCL’s EBITDA/APAT will grow at a CAGR of 37/49% over FY25-30E while RoE will improve from 5.9% in FY25 to 25.4% in FY30E. Q3 EBITDA was 8% below estimates while APAT was 73% below estimates, owing to higher-than expected finance cost. Interest charges were higher owing to cost related to capital deployed for inventory buildup and plant rebuild post fire incident.

Neogen Chemicals Financial Performance

Revenue came in at INR 2,200mn (+9.2/+5.4% YoY/QoQ). EBITDA margin changed by -270bps YoY to 14.5%, owing to higher opex. Organic/inorganic revenue was up 4.3/49% YoY to INR1,870/330mn. The growth in inorganic business was driven by volumes.

Key Con Call Takeaways

(1) Construction of replacement plant at Dahej is on track to be commissioned in Q1. Production ramp from this plant will drive growth in legacy business in ensuing quarters. Non-availability of capacity has compelled NCL to rationalize production and outsource some job work. This has resulted in higher opex cost as well. (2) Pakhajan unit: 30,000 MTPA electrolyte plant shall commence production in Q1 while 3,000MTPA lithium electrolyte salt and additive capacity will commence production in 2HFY27. (3) Dahej Unit: Lithium electrolyte salts and additive capacity of 1,100MTPA and 1,000 MTPA will be commissioned in March-26 and Q1FY27. (4) Neogen Morita New Materials Ltd, a JV between Neogen Ionics and Morita Investment (MIL), is India’s only non‑FEOC compliant plant (Pakhajan unit), offering a China‑alternative supply chain and enabling access to the U.S. 45X tax credit. (5) NCL has received INR0.80bn as an on-account payment from insurance company. Remaining claim amount of INR2.51bn is expected by Q1. (6) USD20mn from MIL for 20% stake will be received by Q1. (7) The board has approved to raise INR1.5bn through preferential issue of equity shares to the promoter group. All these developments shall reduce company’s debt burden. (8) Consolidated and standalone debt stands at INR11.75bn and INR6.8bn. (9) Received provisional approvals for lithium electrolyte salts from several international customers while final site audits underway.

Change in Estimates

We change our estimates for FY26/FY27/FY28 by -61/ 20/+1% to INR 8/27/40x, factoring the increase in finance cost.

Financial Summary (Consolidated)

Change in Estimates (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 13 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.