HSIE Institutional Report: NOCIL Feb, 13 2026

Authored By Prime Research | Published at: Feb 13, 2026 05:19 PM IST

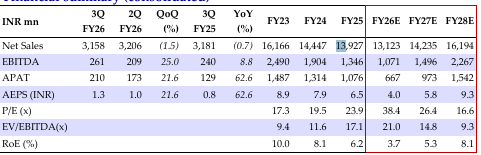

Realization Offsets Volume Driven Growth

Our ADD recommendation on NOCIL with a TP of INR 217 is premised on (1) a shift in product mix toward better-margin specialized rubber chemicals; (2) expected antidumping duty in key products; and (3) capacity addition in coming quarters. Q3 EBITDA/APAT were 14/18% below our estimates, owing to lower-than-expected revenue and higher-than-expected other expenses.

Financial Performance

Revenue was in line with Q2 at INR 3.16bn. Realization remains impacted by pricing pressure due to aggressive dumping by Chinese players while it was partially offset by decrease in raw material prices. EBITDA/KG increased by 23% QoQ to INR 19/KG. EBITDA changed by +8.8/+25 % YoY/QoQ to INR 261mn. EBITDA margin changed by +70/+161bps to 8.3% due to decrease in other expense and raw material cost.

Key Con Call Takeaways

(1) The upcoming revision in US tariff structures is likely to drive volume recovery in the next 2-3 months, while the India‑EU FTA is expected to offer long‑term strategic and raw‑material cost benefits. (2) The company has filed anti‑dumping petitions against China, the EU, the US, Korea, and Thailand, with investigation outcomes are expected in the next 1.5-2 months. (3) The Dahej expansion project is ahead of schedule, with production trials planned for the first half of the year, adding 20% to overall capacity. (4) The company holds a 40% share of the Indian rubber chemical market, estimated at around 85,000 tons.

Change in Estimates

We change our FY26/27/28E EPS estimates by -13.1/ 13.4/-13.3% to INR 4.0/5.8/9.3x to factor in the Q3FY26 performance and growth outlook.

DCF Based Valuation

Our price target is INR 217. The stock is trading at 38.4/26.4/16.6x FY26/27/28E EPS.

Financial Summary (Consolidated)

Change in Estimates (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 13 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.