HSIE Institutional Report: Petronet LNG Feb, 16 2026

Authored By Prime Research | Last Modified: Feb 16, 2026 10:25 AM IST

Kochi Terminal Utilization Improves

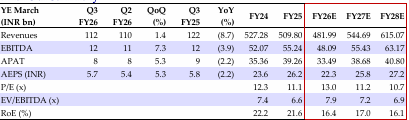

Our REDUCE recommendation on Petronet LNG (PLNG) with a revised TP of INR 275 is based on (1) muted volume growth, (2) delayed capacity expansion, and (3) subdued return ratios resulting from the high capex cycle expected in the next five years. Q3FY26 reported EBITDA of INR 11.98bn (-3.9% YoY, +7.3% QoQ) and PAT of ~INR 8.48bn (-2.2% YoY, +5.3% QoQ), both marginally ahead of our estimates due to lower-than-expected raw material cost. Volumes were at 233tbtu (+2.2% YoY, +2.2% QoQ).

Petronet LNG Financial Performance

Reported EBITDA/PAT stood at ~INR 11.98/8.48bn. Volume at 233tbtu was up 2.2/2.2% YoY/QoQ. PLNG recorded an inventory gain of INR 0.27bn in Q3 against INR 0.41bn in Q2. Other expenses came in at INR 3.34bn as against INR 3.82bn recorded in the previous quarter. As of end-Q3FY26, gross UoP dues stood at INR 13.13bn and provision made amounted to INR 8.15bn, leading to an outstanding balance of INR 4.98bn. Other income came in at INR 2.15bn (+10.1% YoY, -9.0% QoQ) while interest cost was at INR 559mn (-14.1% YoY, -8.3% QoQ).

Terminal Wise Q3 Performance

Utilization at the Dahej terminal was at ~95.9%, while that at Kochi was at ~29.8%. Sales volumes at Dahej and Kochi were 214tbtu (+0.5% YoY, +1.4% QoQ) and 19tbtu (+26.7% YoY, +11.8% QoQ) respectively, resulting in total volume of 233tbtu (+2.2% YoY, +2.2% QoQ).

Conference Call Takeaways

(1) Kochi – Kochi terminal utilization reached its highest level of ~29.8% in Q3FY26 (last four quarters average was ~24%) on account of regassification of cargo brought by MRPL, OMPL, and Kochi Refinery at this location amidst lower LNG prices. Management expects the terminal to be connected to Kochi-Bangalore pipeline by June 2026, which will further increase the utilization of this terminal. Management also noted that once the pipeline construction is completed, the existing capacity of 5MMTPA at this terminal will be insufficient to meet the demand necessitating further capacity expansion. (2) Dahej – additional capacity of 5MMTPA to achieve mechanical completion by March 2026 and construction of the third jetty is expected to be completed in FY27. (3) Capex – ~INR 30+bn worth of capex will be incurred in FY26 (INR 23bn for the petchem plant). Capex will increase to INR 90bn in FY27 which includes INR 75bn for the petchem plant and INR 6bn for construction of the jetty. Capex for the INR 60bn Gopalpur terminal project is expected to be incurred from FY28 onwards as the company awaits environmental clearances.

Change in Estimates and Valuation

We tweak our FY26/27E EPS estimates by +2.1/+1.8% as we reduce raw material cost assumption, owing to weaker crude oil prices. Our TP of INR 275 is based on the Mar-27E cash flow (WACC 11%, terminal growth rate 3%).

Financial Summary

Changes in Estimates

Source: HSIE Research (HSIE Results Daily Report – 16 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.