HSIE Institutional Report: Prince Pipes and Fittings Feb, 12 2026

Authored By Prime Research | Last Modified: Feb 12, 2026 01:03 PM IST

Another Weak Quarter

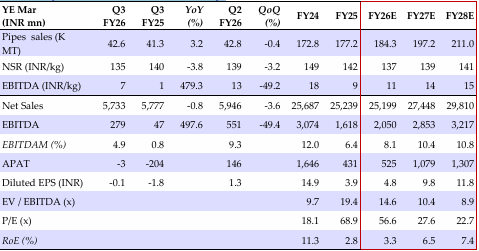

Prince Pipes’ revenue declined 1% YoY due to decline in realization, while plumbing volume grew 3% YoY. EBITDA margin expanded 410bps YoY to 4.9% leading EBITDA to INR 279mn vs INR 47mn YoY, while APAT turned negative owing to higher depreciation. The company booked INR 180-200mn inventory loss in Q3 (3-3.5% of revenue). For FY26, the company maintained its high single-digit volume growth guidance (2% achieved in 9MFY26), with a strong Q4 anticipated. January saw robust double-digit growth, driven by sharp restocking. PVC resin prices increased by INR 11/kg in Q4, aiding channel inventory recovery from depressed levels, though still below normal. We maintain REDUCE with an unchanged TP of INR 260/share by valuing the company at 22x Mar-28 EPS.

Prince Pipes and Fittings Q3FY26 Performance

Revenue declined 1% YoY due to decline in realization (-4% YoY, -3% QoQ). Plumbing volume grew 3% YoY; PVC volumes declined in Q3, while CPVC posted high double-digit growth. EBITDA margin expanded 410bps YoY to 4.9% owing to higher gross margin, decrease in other expenses by 9% YoY, while employee costs increased 5% YoY. EBITDA grew to INR 279mn vs INR 47mn YoY, though APAT turned negative due to higher depreciation. Finance costs stood negative due to interest subvention adjustment of INR 64mn for the Bihar plant. The company booked INR 180 200mn inventory loss in Q3 (3-3.5% of revenue).

Con Call KTAs and Outlook

For FY26, the company maintained its high single-digit volume growth guidance (2% achieved in 9MFY26), with a strong Q4 anticipated. January saw robust double-digit growth, driven by sharp restocking. For FY27, management is targeting double-digit volume growth and EBITDA margins of 10–12%, excluding bathware losses (lowered from the earlier 12% guidance). The company has also ended its partnership with Lubrizol and launched its in-house branded SmartFit Plus CPVC nationwide in December 2025. This moves reduced costs, enabling a 6–7% cut in CPVC pipe prices. The bathware segment is expected to break even by Q3FY27. Considering the rebound in PVC and CPVC resin prices, we have raised our revenue estimates by 3% each for FY26–28E, while maintaining EBITDA forecasts. However, we have increased our FY26E APAT estimate by 10%, reflecting interest subvention benefits from the Bihar plant, with FY27–28E estimates unchanged. We maintain REDUCE with an unchanged TP of INR 260/share by valuing the company at 22x Mar-28 EPS.

Quarterly/Annual Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 12 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.