HSIE Institutional Report: Repco Home Finance Feb, 09 2026

Authored By Prime Research | Last Modified: Feb 9, 2026 11:59 AM IST

Gradual Uptick in Growth Momentum

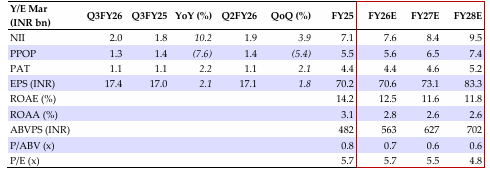

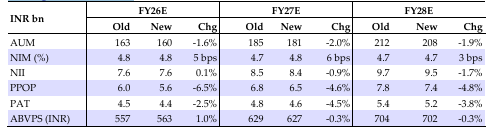

REPCO’s Q3FY26 earnings were marginally lower than our estimates, with negative credit costs (-41bps) offset by higher-than-expected opex. REPCO sustained the momentum in disbursements growth in Q3 (+40% YoY; 28% YoY for 9MFY26) and is on track to achieve FY26 guidance. However, AUM growth remained sub-10% (8.8% YoY) amidst higher run-off rates. New initiatives such as customer sourcing diversification, revamped employee incentives and tech transformation have aided disbursements growth, which had remained subdued in the past. However, profitability amidst credit costs normalization, higher opex structure, and NIMs in declining interest rate environment remains a key monitorable. We revise our FY26E/FY27E/FY28E earnings estimates to factor in lower credit costs offset by higher opex and maintain ADD with a revised RI-based TP of INR570 (implying 0.9x Sep-27 ABVPS).

Mixed P&L Outcomes

REPCO’s NIMs reflated by 10bps QoQ to 5.6%, driven by yield reflation and lower cost of funds. Higher share of non-housing loans aided blended yields, along with ~30bps improvement in cost of funds during 9MFY26. Opex ratios were elevated at 1.97% of AUM (C/I at 36%), partly due to impact of new labor codes and ramp up of distribution network along with higher employee incentives. Profitability moderated sequentially, with RoA/RoE at 2.9%/13.3% respectively.

Improving Asset Quality

REPCO’s GS-III/NS-III improved sequentially to 2.9%/1.4% (Q2FY26: 3.2%/1.5%), with GS-II at 8%. Credit costs remained negative at -41bps, driven by NPA recoveries in the quarter. Adequate provisioning (overall: 2.3%; Stage III: 53%) and strong collections and recovery efforts will likely result in negative credit costs for Q4FY26 as well.

Uptick in Growth Positive Outcome; Balancing Growth-Profitability Key Monitorable

REPCO’s disbursements have witnessed strong traction during 9MFY26. With several initiatives such as expansion of the distribution footprint, separate sales and credit verticals, new sourcing channels and technology upgrades, REPCO has multiple levers to sustain the growth momentum to drive AUM growth above 12% during FY27-FY28E. However, sustaining profitability amidst credit costs normalization, higher opex structure and NIMs, while maintaining the strong growth momentum amidst elevated competitive intensity and moderate housing demand remains a key monitorable for meaningful rerating.

Repco Home Finance Financial Summary

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 09 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.