HSIE Institutional Report: Route Mobile Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 01:00 PM IST

Focus on Higher Margin Business; Valuations Attractive

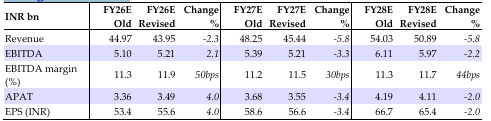

Route Mobile’s Q3 performance was defined by a strategic transformation toward higher-margin business, resulting in a gross profit margin expansion to 24.5% (+340/243bps improvement YoY/QoQ). While revenue witnessed a 6.5% YoY and 1.1% QoQ decline due to a deliberate shift away from low-margin ILD messaging, absolute gross profit grew 8.6% YoY. The company’s growth strategy emphasizes on high-margin OTT solutions like WhatsApp and RCS (new products revenue grew 14.5% YoY for 9M) alongside specialized telco offerings such as firewalls and network API platforms through the Konera initiative. Domestic messaging trends show improvement, but it has a lower price points compared to international business and require higher volumes but yield superior margins. To propel future growth Route Mobile is leveraging its partnership with Proximus Global and global SIs like Infosys and TechM. This strategic direction is further strengthened by the elevation of Tushar Agnihotri as the new CEO, who brings over 30 years of experience. We reduce our revenue estimate by ~5-6% to factor business shifts but increase margins leading to ~2-3% cut in EPS. We maintain our ADD with a TP of INR 885, based on 14x Dec-27E EPS. The stock is trading at a PE of 10/9x FY27/28E EPS and generates a RoE of ~15% for FY25.

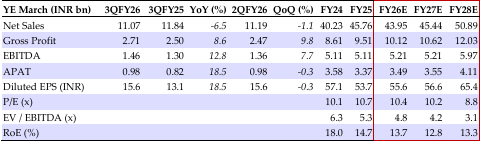

Route Mobile Q3FY26 Highlights

Revenue grew -1.1/6.5% QoQ/YoY to INR 11.07bn (vs our estimate of INR 11.52bn) due to a decline in ILD messaging volumes although partially offset by rise in domestic business growth. Gross profit margin expanded by 243bps QoQ to 24.5%, marking the highest level in the past eight quarters. New product sales declined 3.9% QoQ to INR 902mn. Reported EBITDA increased 7.7% QoQ to INR 1.46bn, and the EBITDA margin improved by 108bps QoQ to 13.2%, materially lower compared to the gross margin expansion of 243bps, mainly led by an increase in other expenses by 29.4% QoQ. Finance costs stood at INR 0.01bn, down by 40.1% QoQ. Revenue from India terminations (~47% of revenue) declined 13.8% YoY and international revenue increased 1.2% YoY. Net cash stood at INR 12.88bn, ~36.5% of the market cap.

Outlook

We expect +8/9% revenue/EPS CAGR for FY26-28E, led by 3.9/+3.4/+12.0% revenue growth and 11.9/11.5/11.7% EBITDA margin for FY26/27/28E respectively.

Quarterly Financial Summary

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.