HSIE Institutional Report: Samvardhana Motherson International Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 10:37 AM IST

Operational Improvement to Continue

The company continues to well execute its strong order book, with a focus on improving the operational performance further in the coming quarters. The aerospace and consumer electronics business continues to grow well, as the company also expands its product portfolio. The company has many plants globally, and believes in local for local, which has largely protected it from direct impacts of higher tariffs. However, there has been indirect impact via customers. Now with the US tariff situation becoming clearer globally and the India EU FTA benefits coming in, we expect the company to benefit from improved planning at the customers’ end. Additionally, given continuing global demand headwinds, supplier distress, and company’s strong balance sheet, we expect it to close in on acquisition/s, now that the US tariff scenario is becoming less foggy. Considering the positives, we value SAMIL at 22x Dec 27 EPS (from 21x earlier) for a TP of INR 142 and maintain ADD.

Samvardhana Motherson International Quarterly Performance

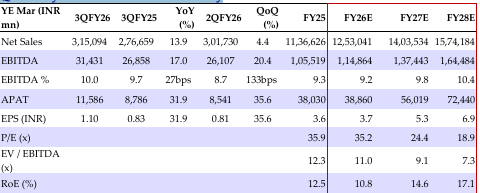

EBITDA margin at 10% was up 27bps YoY and 132bps QoQ, 113bps above our estimate and 94bps above Bloomberg consensus estimate. Margin improvement QoQ was led by the Integrated Assembly division as well as the Modules and Polymer Products division. Revenue grew 13.9% YoY to INR 315.1bn, also aided by the Asumitec acquisition.

Earnings Call Takeaways

(1) Margins were aided by benefits from favorable forex and savings from transformative measures being undertaken in the European operations. (2) Outlook for the global PV production is positive, estimated at 93mn units in FY27 from an estimated 91mn units in FY26. (3) The consumer electronics business is ramping up as planned (grew 75% QoQ) with two plants already operational, while a third one is expected to commence operations in Q3FY27, which should double the capacity of the division. (4) The aerospace business grew 40% YoY with the order book seeing sustained growth, supported by product portfolio expansion. (5) It has also secured government incentives under the ECMS scheme which will further support scalability, competitiveness, and long-term profitability. (6) The integrated assembly division’s performance is being aided by the group strength where the company is also doing more manufacturing to support the customer’s operations. (7) It has planned two more greenfield plants (one for vision systems in India and the other for wiring harness in Morocco), taking the total greenfield plants to 12 now, across emerging markets, spanning both auto and non-auto segments. (8) Capex guidance stands at INR 60bn (+/- 10%) for FY27.

Quarterly/Annual Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.