HSIE Institutional Report: Sansera Engineering Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 11:32 AM IST

Impressive Traction in the Non-Auto Segment

The Aerospace, Defense, and Semiconductor (ADS) segment continues to perform well, and is at an inflection point—margin accretive and a key driver of diversification beyond the auto Internal Combustion Engine (ICE) business. The company has improved its capability to provide complex parts in the aerospace segment, while it is seeing huge potential in the semiconductor space, having already acquired a major customer. Additionally, while it is diversifying, it is also mindful of opportunities to juice the auto ICE segment, and is working to capitalize on the trend of OEMs seeking to outsource crankshaft assemblies. Considering the interim trade deal between India and the US (US forms ~9% of revenue), as well as the India EU FTA, it would help reduce uncertainty as well as create opportunities. However, it is awaiting the final signing and fine print of the India-US trade deal for clarity on the exact tariff and regional content value, to decide on setting up a plant in the US. Considering improving visibility of good growth in the medium to long term, which is also led by improving product mix, we revise our financials upward and increase our target multiple from 24x earlier to 28x Dec-27 EPS for a TP of INR2,443 and upgrade to a BUY rating.

Quarterly Performance

Consolidated EBITDA margin at 18.1% was up 60bps YoY and 72bps QoQ, 19bps above our estimate and 46bps above the Bloomberg consensus estimate. This was led by higher growth in the ADS segment and thus in turn the exports segment, with the ADS segment forming 13.9% of the mix in Q3FY26 (vs 6.4% in Q2FY26 and 4% in Q3FY25).

ADS Segment at an Inflection Point

Revenue for the segment stood at ~INR 1.19bn in Q3FY26, registering a growth of 344% YoY and 141% QoQ. Its current order book stands at INR 38.7bn with good visibility until FY30. It has one major customer in the semiconductor segment and is in active dialogue with others too, and sees huge potential in the segment.

New Plant for Crankshafts

Inauguration of the new and highly automated plant is expected in Feb 2026, where the company will focus on crankshafts and crankshaft assemblies, with a focus to cater to domestic 2W OEMs. It highlighted that more than half the OEMs are assembling crankshafts in house and are looking at gradually outsourcing the same.

Other Key Drivers

1) It indicated that based on production schedules, it expects to see sustained growth in the coming months. 2) New model launches are aiding the domestic business. 3) Considering the order book, it expects a steep ramp-up in revenue over FY28-FY30. 4) It is seeking to supply to the energy business as well as for humanoids and autonomous car segments of a large North American EV customer.

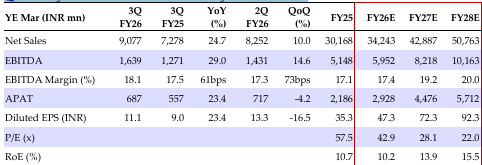

Quarterly/Annual Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.