HSIE Institutional Report: Shree Cement Feb, 09 2026

Authored By Prime Research | Last Modified: Feb 9, 2026 11:22 AM IST

Focus on Value Drives Pricing Gains Amid Op-Lev Loss

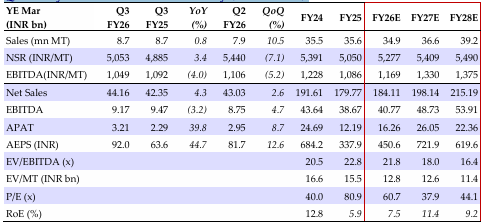

We maintain ADD on Shree Cement (SRCM) with a lower SOTP target price of INR 29,000/share (India operations at 16.5x FY28E EBITDA, UAE operations at 3x BV). In Q3FY26, SRCM’s India sales rose a modest 1% YoY (-1% YoY in 9MFY26). Continued focus on value over volume drove up its cement NSR by 2% YoY, while peers reported a decline! However, blended unit EBITDA (INR 1,049/MT) fell INR 43/MT YoY, mainly on op-lev loss.

Shree Cement Q3FY26 Performance

Sales volume rose a modest 1% YoY to 8.7mn MT. While blended NSR fell 7% QoQ, cement NSR fell 4% QoQ (weak pricing and fall in trade sales share to 65% vs 70% QoQ). SRCM noted that is has been focusing on bridging the price gap vs market leader UltraTech, at the expense of losing market share. This has indeed resulted in SRCM delivering NSR gain of INR 100/MT YoY vs NSR decline of INR 50/MT by market leader. Unit EBITDA fell INR 60/MT QoQ to INR 1,049/MT on weak pricing. Fuel cost rate fell marginally to INR 1.56/mnCal vs INR 1.66 QoQ. Low-cost green power share remained flattish at 60% QoQ. Lead distance also stood flattish at 446km vs 441km QoQ. While standalone revenue rose 4% YoY, EBITDA fell 3%. Consolidated revenue/EBITDA rose 5/4% YoY on higher contribution from UAE subsidiary. SRCM spent INR 6.5/15bn in capex during Q3/9MFY26.

9MFY26

Standalone volume fell 1% YoY, significantly lagging the industry as SRCM continued its thrust on better pricing over volume. Thus, blended unit EBITDA rose INR 228/MT YoY to INR 1,180/MT on better pricing, rising share of premium sales, strong value focus and lower energy costs. Standalone revenue/EBITDA rose 7/23% YoY (on better pricing and margin) and consolidated revenue/EBITDA jumped 8/33% (additional contribution from improvement in UAE’s profitability).

Outlook

SRCM’s Q4FY26 volume guidance of ~9.5mn MT implies FY26 volume would fall 3% YoY (as against earlier guidance of +4% growth). The Karnataka expansion is expected to be operational in Q4FY26, increasing its Indian capacity to 69mn MT. Additionally, it is also expanding the UAE cement capacity by 3mn MT, to ride on real estate buoyancy in the country. We reduce our FY26/27/28E EBITDA estimates by 8/6/9%, factoring in slower volumes (FY25-28E CAGR of 3% vs 6% earlier) and lower margin in FY26E.

Quarterly/Annual Financial Summary (Standalone)

Source: HSIE Research (HSIE Results Daily Report – 09 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.