HSIE Institutional Report: Star Cement Feb, 10 2026

Authored By Prime Research | Last Modified: Feb 10, 2026 01:11 PM IST

Stellar Performance Continues Quarter After Quarter

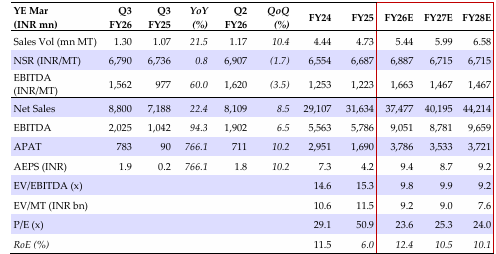

We maintain BUY on Star Cement with an unchanged TP of INR 290/share (12x FY28E consolidated EBITDA). Star continues to shine, riding on the benefits of duopolistic position in the lucrative NE region (NER), along with high incentive accruals from recent expansions. Its profitability also benefits from cost controls and rising share of green energy. In Q3FY26, Star’s solid volume performance continued: +22% YoY. Despite a fall in incentive accruals by INR 184/MT QoQ and weak pricing, unit EBITDA fell a modest INR 57/MT QoQ and remained industry best at INR 1,562/MT. Star’s plans include near doubling its capacity over the next four years as it is expanding capacity in Assam and is setting up greenfield capacities in Bihar, Rajasthan, and Haryana. It will raise equity capital to part-fund the same to keep leverage under control.

Star Cement Q3FY26 Performance

Consol volume rose 22% YoY, aided by higher clinker sales while cement volume rose 16%. Cement sales in the NER firmed up 13% YoY and outside NER volume rose 28% YoY. Incentive accrual reduced to INR 293/MT vs INR 477/MT QoQ, post the reduction in GST rate w.e.f. Sep 25. This along with fall in cement prices drove down NSR by 2% QoQ. The fall appears lower owing to higher sales QoQ in higher-priced NER. Opex fell 1% QoQ on op-lev gain (+10% QoQ volume rise) which more than offset for 6% higher logistics cost (trucks freight cost went up in Meghalaya). Thus, unit EBITDA cooled off a modest INR 57/MT QoQ to INR 1,562 (+INR 586 YoY despite lower incentives).

Outlook

STRCEM’s Q4FY26 volume guidance implies FY26 growth at a robust 17%. It also expects strong growth in FY27E on continued capacity ramp-up. It also noted that cement prices have remained flat vs Q3FY26 exit. STRCEM lowered FY26 capex guidance to INR 5.8bn and will share FY27 capex guidance later as it is finalizing its north expansion plan. The 2mn MT SGU at Silchar is due for commissioning in Q4FY26. STRCEM plans to set up 2mn MT SGU in Bihar by FY28. The Jorhat SGU will be taken up later along with a greenfield plant in Assam. As per earlier guidance, it is also acquiring mining and plant land in Jaisalmer to set up IU for an investment of INR 20 25bn (estimated by late FY29). We raise FY26E EBITDA estimates by 4%, factoring in healthy performance. We maintain our FY27/28E EBITDA estimates. We estimate consolidated volume/EBITDA/APAT CAGR of 12/19/30% for FY25-28E.

Quarterly/Annual Financial Summary (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 10 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.