HSIE Institutional Report: State Bank of India Feb, 09 2026

Authored By Prime Research | Last Modified: Feb 9, 2026 11:42 AM IST

Productivity Gains to Drive Earnings Reflation

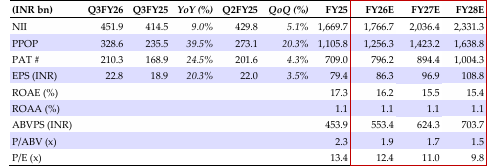

SBIN’s Q3FY26 earnings beat estimates on the back of healthy growth on both sides of the balance sheet, stable margins, in-line asset quality, and interim dividend from SBI Funds management (~INR2.2bn). Loan growth (+15% YoY) continued to outpace the system, led by pick-up in the corporate segment, even as growth in RAM segments remained strong. Deposit growth (+9% YoY; 2% QoQ) was relatively soft, while the CASA ratio declined to 37.5% (-46bps QoQ), with softer traction in CA balances. Credit costs and gross slippages trended lower, with asset quality continuing to improve across asset classes. We believe SBIN is likely to sustain its productivity and efficiency gains, coupled with stable asset quality, driving sustainable ROAs at 1.1%. We maintain BUY with a SOTP-based revised TP of INR1,200 (standalone bank at 1.5x Sep-27 ABVPS); reiterate SBIN as the top pick amongst PSU banks.

Strong Growth Coupled with Stable Margins

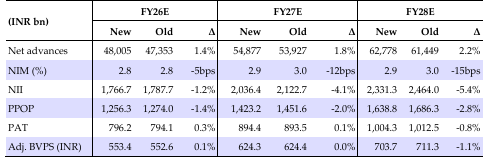

Healthy NII growth (+9% YoY) was driven by lower cost of deposits (-8bps QoQ), offset by lower asset yields (-7bps QoQ), translating to stable margins at 2.95%. Strong loan growth (+15% YoY; 6% QoQ) was led by growth across asset classes, with significant pick up in wholesale banking credit (+7% QoQ). We build 14.5% loan book CAGR during FY26-28E, with pick-up in credit growth across asset classes.

Benign Asset Quality

Gross slippages clocked in at 0.4% (Q3FY25: 0.5%), with stable recoveries and lower SMA balances. Credit costs trended lower to 29bps (Q2FY26: 39bps), as credit quality remained benign across portfolios. Going forward, we believe the asset quality shall continue to remain benign and build in average credit cost of ~45bps for FY27/FY28E.

Operating Leverage to Drive Earnings Reflation

Given its competitive moats (largest distribution network and continued investment in technology and people), SBIN is chasing productivity (throughput) and efficiency gains (fee income and opex) to drive medium-term RoAs above 1.1%.

State Bank of India Financial Summary

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 09 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.