HSIE Institutional Report: Tata Motors Passenger Vehicles Feb, 06 2026

Authored By Prime Research | Last Modified: Jun 9, 2026 03:03 PM IST

JLR’s Challenges Continue, Albeit Restocking to Support Q4

Besides weak demand globally, Jaguar Land Rover (JLR) is also facing structural headwinds from its business in China as JLR’s addressable market gets disrupted by a higher luxury tax at the top end of its portfolio and by strong competition from Chinese OEMs at the lower end. Considering China has been a highly profitable market for the company before, we expect both volume and margin expansion to be capped, going forward. What this is also doing is shifting focus of the Chinese OEMs burdened with overcapacity to focus on markets outside China (besides US), which we believe could keep Variable Marketing Expense (VME) higher at mid-single digits for JLR. Considering these challenges that have also been worsened by higher tariffs of exporting to the US, management declined to give an outlook of FY27, deferring it to the investor day in June 2026. However, considering the restocking opportunity post the cyber-attack incident, Q4 should be a good quarter for JLR in the midst of otherwise challenging times. The India PV segment continues to do well and is expected to benefit from the ramp-up of Sierra’s sales, and thus benefit from higher operating leverage and improved mix. We value the company on a SOTP basis, with JLR valued at (INR 140) 2.25x Dec-27 EPS, the India PV business valued at (INR 206) 23x Dec-27 EPS, and the stake in Tata Technologies valued at INR 30, for a target price of INR 376 and maintain a REDUCE rating.

JLR Quarterly Performance

EBIT margin in Q3 at negative 6.9% was better than our estimate of negative 10.8%, a slight recovery from the negative 8.6% margin in Q2. However, Q4 is expected to be a much better quarter, considering channel filling opportunity, aided by normalized production.

JLR Guidance

Management held on to its FY26 guidance for EBIT margin to 0-2%, and for free cash flow to be negative £2.2bn-negative £2.5bn. However, it held back from giving a guidance for FY27 despite hinting in the Q2 earnings call that there would be better visibility by the time of Q3 results. It indicated that 2026 should see the launch of the Range Rover electric, unveiling of the production-ready new Jaguar, and start of production of Freelander.

India PV Update

EBITDA margin at 4.3% was below our estimate of 6%. It expects the company to continue outgrowing the domestic PV industry, aided by Sierra’s volumes, which it indicated was 7k dispatches in Jan 2026, with an order book running into six digits. While it avoided a price hike in Jan, it seeks to take it in Feb, mainly to pass on higher commodity costs. Going forward, margin should benefit from operating leverage, cost optimization, and better product mix on ramp-up of Sierra, Harrier petrol, and Safari petrol. It highlighted supply challenges as suppliers, especially casting suppliers as they are working at high utilization levels. It mentioned that it is seeking to expand the PV capacity in two phases over the next 5-6 months.

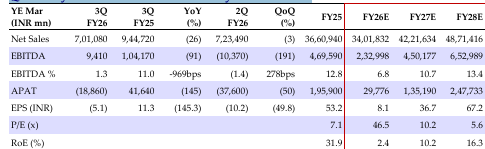

Quarterly/Annual Financial Summary

Source: HSIE Research (HSIE Results Daily – 06 Feb 26 – HSIE-202602060713371815208.pdf)

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.