HSIE Institutional Report: Tata Steel Feb, 09 2026

Authored By Prime Research | Last Modified: Feb 9, 2026 11:30 AM IST

Margin to Gain as Prices Recover; Demand Remains Firm

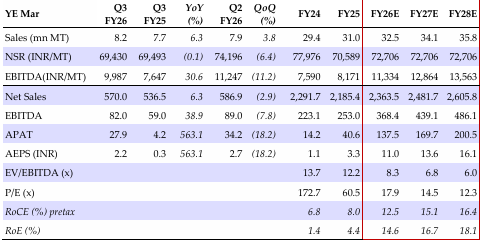

We maintain BUY on Tata Steel with a revised TP of INR 220/share (6.5x its FY28E consolidated EBITDA). Tata Steel’s consolidated volume growth of 6% YoY benefited from industry-leading 14% growth in India, while EU volumes declined. Weak pricing and higher coking coal prices pulled down unit EBITDA by INR 1.3k/MT QoQ to INR 10k/MT. We estimate consolidated volume/EBITDA to grow at 5/24% CAGR during FY25-28E, driven by rebound in recent domestic steel prices, expected uptick in EU prices, continued cost reduction efforts across all units, and volume ramp-up.

Tata Steel Q3FY26 Performance

Consolidated volumes rose 6% YoY, driven by 14% jump in domestic sales while EU sales declined 9% YoY. Domestic/blended NSR slumped 6/6% QoQ on continued fall in steel prices in Oct/Nov. Even coking coal cost rose USD 4/MT QoQ, adding to gross margin compression. Profitability fell QoQ in India and the Netherlands and the UK continued to operate in EBITDA losses. Tata noted that the cost-cut program drove opex reduction by INR 31bn in Q3 (India/UK/NL INR 9/6/16bn respectively) vs INR 26bn in Q2FY26. Thus, consolidated unit EBITDA fell INR 1.3k/MT QoQ to INR 10k/MT. Another INR 30bn targeted cost savings are expected over the next few quarters.

Con Call KTAs and Outlook

Tata affirmed Q4 average realization could increase by INR 2.3k/MT (safeguard duties benefit) vs INR 2.1k/MT fall in Q3. However, the gains would largely be offset by ~USD 15/MT rise coking coal prices. The management noted that as EU has moved CBAM from a report only phase to definitive regime Jan-26 onwards, domestic steel prices in Europe will gradually increase in 2026 and even imports will reduce. Tata is also expecting import quota restrictions to happen in the UK, which should support regional pricing and profitability. Tata noted it is bound to both deliver volume growth and rising share of value-added downstream projects to bolster its profitability. It expects steel prices to recover in India and the Netherlands in the coming months. UK prices will recover once the government trims import quotas. Tata Steel would continue to lower costs thorough its cost transformation program across plants. The EAF plant in Ludhiana (0.8mn MT) will be operational by Mar-26E driving growth. It is working on other expansion projects in India and Europe to 40mn MT by 2030E. We have marginally increased FY26/27/28E consolidated EBITDA by 2/2/1%, factoring in price recovery.

Quarterly/Annual Financial Summary (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 09 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.