HSIE Institutional Report: Teamlease Services Feb, 05 2026

Authored By Prime Research | Last Modified: Feb 5, 2026 02:14 PM IST

Client Headwinds Behind, Focus on Profitable Growth

TeamLease reported a mixed quarter with strong EBITDA growth of 10.5% QoQ (~22.8% YoY in 9MFY26) and consolidated margin expansion of 14bps QoQ, while revenue declined 0.6% QoQ due to a sharp drop in associates for a BFSI staffing client, following employee insourcing, led by regulatory changes. General staffing (GS) and Degree Apprenticeship (DA) headcount fell by ~27K (the highest quarterly decline) due to this client-specific event, which management indicated is now behind, with headcount expected to recover in Q4FY26E. The HR segment grew 8.9% QoQ and turned profitable with a 7% margin, with 4Q expected to be the strongest quarter for margins. Specialized Staffing (SS) growth was led by GCCs, which now contribute ~65% of SS revenue; margins for SS are expected in the 6–7% range, with new GCC additions driving further growth. The company incurred a one-time labor expense of ~INR 57mn related to the change in labor code. Margin expansion efforts remain focused on operating leverage, group-level cost optimization, and better portfolio mix. While the full benefit of new labor codes will take time to reflect, achieving 25% EBITDA growth for FY26E appears challenging; however, we have assumed FY26E EBITDA growth of ~19% YoY. We retain our EPS estimate and retain BUY with a TP of INR 2,200, based on 20x Dec-27E EPS.

Teamlease Services Q3FY26 Highlights

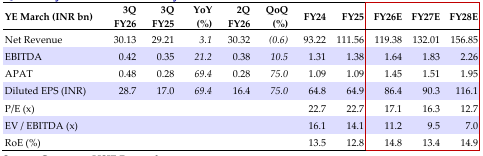

Consolidated revenue stood at INR 30.13bn, -0.6/+3.1% QoQ/YoY, due to a -1.0/+2.0/+8.9% QoQ increase in GS/SS/HR revenue. The GS PAPM improved to INR 680 (vs INR 669 in Q2), and the associate/core ratio decreased to 355 (-7.1% QoQ) due to drop in associates. Funding exposure remains at 14% along with DSO at 7 days. EBITDA margin for GS/SS/HR stood at 1.1/6.5/7.0%. 22 new logos were added in GS and 55% of new clients were added on variable markup; this will help in PAPM growth. SS headcount increased by 115 (~22 from TLD Global), as GCCs continued to display strength. GCCs are ~65% of SS revenue (vs 60% in Q2). 17 new logos were added in the DA segment. Net cash stood at INR 4.30bn (~17.1% of market cap).

Outlook

We expect revenue growth of 7/11/19% and an EBITDA margin of 1.37/1.38/1.44% in FY26/27/28E, leading to revenue, EBITDA, and EPS CAGRs of 12%, 18%, and 21% over FY25-28E.

Quarterly Financial Summary

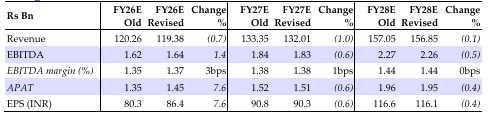

Change in Estimate

Source: HSIE Research (HSIE Results Daily – 05 Feb 26 – HSIE-202602050642042086559.pdf)

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.