HSIE Institutional Report: The Ramco Cements Feb, 10 2026

Authored By Prime Research | Last Modified: Feb 10, 2026 12:01 PM IST

Subdued Volumes; Margin at a 13-Quarter Low!

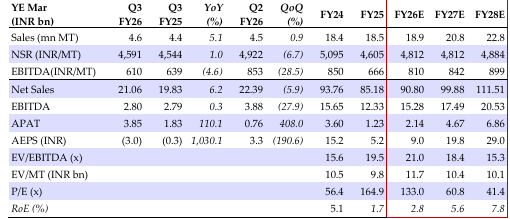

We maintain SELL on The Ramco Cements (TRCL) with a lower target price of INR 920/share (12x FY28E consolidated EBITDA). TRCL’s subdued profitability should keep its leverage high (we estimate net debt to EBITDA will remain >2x during FY26-27E) and return ratios low. In Q3FY26, TRCL’s volume growth remained subdued at ~5% YoY. Even NSR fell 7% QoQ which dented margin to a 13-quarter low of INR 610/MT. We estimate its consolidated volume/EBITDA will grow at 7/19% CAGR during FY25-28E.

Ramco Cements Q3FY26 Performance

TRCL’s sales volume rose a modest 5/1% YoY/QoQ. Cement sales in the south rose 5% YoY while it fell 1% in the east. Trade share stood at 67% vs 69/67% QoQ/YoY. Overall premium sales’ share stood at 28% vs 25/29% YoY/QoQ. NSR fell sharply: down 7% QoQ on price correction across south and east. Unit opex fell 2% QoQ owing to lower employee and other expenses while its fuel cost rate increased by ~INR 40/MT and green lower share remained flattish. Lower NSR thus pulled down unit EBITDA by INR 243 to INR 610. On a YoY basis, despite 1% higher NSR, unit EBITDA fell by INR 29/MT due to the impact of increased royalty on limestone mining in Tamil Nadu and higher fixed costs. Net debt to EBITDA remained elevated at 3x in Dec’25 vs 3.3x QoQ.

Other Updates and Outlook

TRCL spent INR 2.22/8.23bn in gross capex in Q3/9MFY26. It would spend INR 2.8bn in Q4FY26. Its planned expansion to 30mn MT is delayed and is expected to be fully completed by the end of FY27. Factoring in disappointing performance in Q3FY26, we have lowered our EBITDA estimates by 3/8/8% respectively. We estimated consolidated volume/EBITDA CAGRs of 7/19% respectively. Amid lower profitability, we have deferred its Karnataka expansion to FY29E. We have modelled cumulative capex of INR 34bn for FY26-28E. We estimate net debt to EBITDA will reduce gradually to 2.8/2.4/1.9x in Mar’26/27/28E from 3x currently.

Quarterly/Annual Financial Summary (Consolidated)

Source: HSIE Research (HSIE Results Daily Report – 10 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.