HSIE Institutional Report: Thermax Feb, 06 2026

Authored By Prime Research | Last Modified: Feb 6, 2026 02:28 PM IST

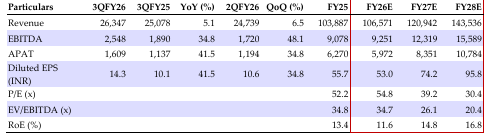

Marginal Beat on Numbers

Thermax Ltd (TMX) reported revenue/EBITDA/APAT of INR 26.3/2.5/1.6bn, a beat/miss by -2.3/+5.9/+4.6%. The EBITDA margin of 9.7% was higher than our estimate of 8.9%, largely due to improvement in operational efficiency and receding low margins legacy projects. Order inflow in Q3FY26 witnessed a 34% uptick YoY at INR 30.8bn, taking the OB as of Dec’25 to INR 126.4bn (+11%YoY). The performance in Industrial Products segment is lower due to product mix. Profitability in the Industrial Infrastructure segment is higher this year on account of increased operational efficiency. Last year’s numbers reflected a project cost overrun, which impacted margins. Chemicals segment profitability is lower due to fixed cost of a new plant and change in product mix. Green Solutions business has margin improvement due to operational efficiency and one the of the subsidiaries has received insurance claim proceeds. New growth drivers are emerging in the form of Data Centre solutions, medium MW power projects, utility power projects, ramp-up of the chemical business, and increased traction in products launched over the past few years. Profitability continues to improve with changes in mix toward profitable industrial products and completion of lower-margin order backlog. Ramping up of new product portfolio, impetus on cleaner air and water, and focus on bio-CNG will be add ons. We have cut estimates, given weak execution of order book. We maintain BUY on TMX, with a TP of INR 4,175 (45x Dec-27E EPS rollover).

Q3FY26 Financial Highlights

Revenue: INR 26.3bn (+5.1/-6.5% YoY/QoQ, miss by 2.3%); industrial products/industrial infra/green sol/chemical posted growth/decline of +19/-9/-14/+5% YoY. EBITDA: INR 2.5bn (+34.8/+48.1% YoY/QoQ, a beat by 5.9%), with EBITDA margin of 9.7% (+213.6/+271.8bps YoY/QoQ, vs our estimates of 8.9%). EBIT margin: industrial product: 9.3% ( 199.3/-60.6bps YoY/QoQ); industrial infra: 6.3% (+622.2/+790.3bps YoY/QoQ); green solution: 5.2% (+632.2/-89bps YoY/QoQ); chemical: 4.6% (-916.5/-519bps YoY/QoQ). APAT stood at INR 1.6bn (+41.5/+34.8% YoY/QoQ, a 4.6% beat).

Expect Double Digit Base Order Growth; Large Orders to Make a Comeback

Order booking is improved on the back of improved performance in export in the MENA region, including data centre infrastructure solutions, utility boilers and associated systems for Nigeria project. F&B orders increased although Sugar/Distillery dropped which historically is a leading contributor. Data centre is emerging as a new sector with tremendous future potential. Order booking is expected to grow 20% YoY.

Consolidated Financial Summary

Change in Estimates (INR mn)

Source: HSIE Research (HSIE Results Daily Report – 06 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.