HSIE Institutional Report: Titan Feb, 12 2026

Authored By Prime Research | Last Modified: Feb 12, 2026 01:27 PM IST

Jewelry Momentum Remains Strong

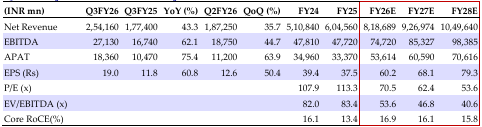

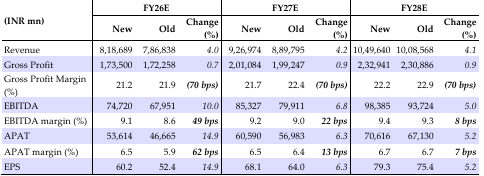

Consolidated jewelry sales (ex-bullion and digi gold) grew 42.1% YoY to INR225.2bn (in-line), driven by gold price-led increase in ABV but partially offset by flat buyer growth. Domestic jewelry (ex-bullion and digi gold sales) grew 40.5% YoY (consolidated topline growth stood at 43.3% YoY at INR 254.2bn; HSIE: 248.4bn). Consolidated jewelry EBITM (ex-bullion) expanded by 159bps to 11% (HSIE: 9.3%), aided by a low base. Note: Q3FY25 had INR2.53bn customs duty impact on EBIT in Tanishq/Mia/Zoya (TMZ). Adjusted jewelry EBITM (ex-bullion) would have been flat YoY at 11%. The company continues to leverage its gold exchange program to sustain footfalls. Non-jewelry segment grew 20.5% YoY to INR19.8bn (HSIE: 18.7bn), with margins up 174bps YoY to 9.6% (HSIE: 9.3%). Management recommended that EBIT growth may be a better KPI to track than EBITM in a persistently rising gold price environment. We have revised our FY27/28 EPS estimates upward by 5-6% to account for higher revenue growth. We maintain our REDUCE rating with a DCF-based TP of INR4,000/sh (implying 50x Mar-28 P/E).

Titan Q3FY26 Highlights

Consolidated revenue grew 43.3% YoY to INR 254.2bn. Consolidated jewelry (ex-bullion and digi gold) sales grew 42.1% YoY to INR225.2bn (in-line). Domestic jewelry (ex-bullion and digi gold) sales grew 40.5% YoY in Q3FY26, driven by gold price-led increase in ABV but partially offset by flat buyer growth. New buyer contribution stood at 45% in Q3FY26 (vs 48% in Q3FY25) and jewelry ABV stood at INR0.19mn in Q3FY26 (plain gold/studded ABV up 44/15% YoY). The company continues to leverage its gold exchange program to sustain footfalls. Plain gold jewelry grew 37% YoY on the back of wedding demand and gold coins, while studded jewelry grew by 26% YoY. Studded ratio stood at 26% in Q3FY26 vs 28% in Q3FY25. Jewelry EBITM (consolidated) expanded by 159bps to 11% (HSIE: 9.3%), aided by a low base (note: Q3FY25 had INR2.53bn customs duty impact on EBIT in TMZ; adjusted EBIT for TMZ grew ~34% YoY). Watches/eyewear/others grew ~14/18/47% YoY respectively. The non-jewelry segments EBITM expanded by 174bps YoY to 9.6% (HSIE: 9.3%). The company added 12/11/1/24/1 Tanishq/Mia/Zoya/Caratlane/BeYon stores (net) respectively in Q3. Consolidated APAT grew 75.4% YoY to INR 18.4bn (HSIE: INR 14.4bn).

Outlook

We’ve realigned our FY27/28 EPS estimates by 5-6% to account for higher revenue. However, tough comparables (courtesy high gold price base) may weigh heavy on jewelry growth in FY27 and remains a key monitorable. We maintain our Reduce rating with a DCF-based TP of INR4,000/sh (implying 50x Mar-28 P/E).

Quarterly Financial Summary

Change in Estimates

Source: HSIE Research (HSIE Results Daily Report – 12 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.