HSIE Institutional Report: Trent Feb, 05 2026

Authored By Prime Research | Last Modified: Feb 5, 2026 02:26 PM IST

Margins Continue to Surprise Positively

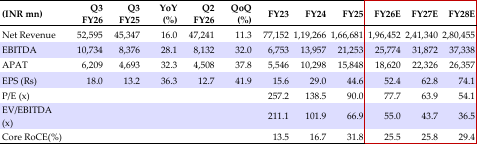

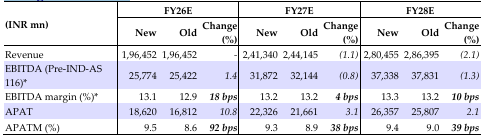

Standalone revenue growth moderated to 16% YoY at INR 52.6bn due to headwinds from muted consumer sentiment and a shift in the festive calendar. Fashion formats reported a slightly negative SSSG in Q3 (9MFY26 SSSG was in low-single digits). As highlighted in our Jan-26 report, the company has pivoted expansion from saturated South+West to relatively untapped North+East markets. While consumption density may take time to mature, these under-retailed territories offer significant growth/SSSG potential. Trent added 17/48 (net) stores of Westside/Zudio respectively. Its grocery format Star grew by 1% YoY. The company continues to surprise on margins – GM/EBITDAM expanded by 29/194bps YoY to 45/20.4% in Q3 (HSIE: 43.3/18.1%), led by cost optimization and operational efficiencies. Pre-IND AS EBITDAM improved by ~60bps to 13.8% this quarter (vs 13.2% in Q3FY25). We marginally increase our FY27/28 APAT estimates by 2-3% to account for better Zudio margins and maintain ADD with SOTP-based TP of INR 4,700 (including 60x FY28 P/E for standalone business and 3x FY28 EV/sales for Star).

Q3FY26 Highlights

Standalone revenue grew by 16% YoY to INR 52.6bn. Growth was impacted by muted consumer sentiment and a shift of festive season. Growth was primarily led by new store additions as LFL growth stood marginally negative in Q3FY26. Westside/Zudio added 17/48 stores in Q3FY26, taking their total store count to 278/854 respectively. In Zudio, over 75% of new stores additions in 9MFY26 were in Tier 2/3 cities and emerging micro-markets. Westside’s online revenue surged 38% YoY, accounting for over 6% to Westside’s revenue. Star revenue grew by 1% YoY to INR 8.96bn. Staples/FMCG/Fresh/GM&A grew by 1/1/13.6/-4.8% YoY in Q3FY26. Standalone GM improved by 29bps YoY to 45% (HSIE: 43.3%). Consequently, EBITDAM expanded by 194bps YoY to 20.4% (HSIE: 18.1%), driven by manpower cost optimization. However, management noted that the manpower efficiency gains, driven by RFID implementation, have now largely been realized. Operating EBIT margin stood at 13.8% in Q3FY26 vs 13.2% in Q3FY25. EBITDA/APAT grew 28.1/32.3% YoY to INR 10.7/6.2bn (HSIE: INR 9.4/4.7bn).

Outlook

We suspect Trent’s (1) incremental expansion toward under-retailed territories of North and East, (2) step-up in Westside store and member additions are likely to aid a SSSG recovery in the future. We marginally increase our FY27/28 APAT estimates by 2-3% to account for better Zudio margins and maintain our ADD rating with SOTP-based TP of INR 4,700 (including 60x FY28 P/E for standalone business and 3x FY28 EV/sales for Star).

Quarterly Financial Summary (Standalone)

Change in estimates

Source: HSIE Research (HSIE Results Daily – 05 Feb 26 – HSIE-202602050642042086559.pdf)

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.