HSIE Institutional Report: Zydus Lifesciences Feb, 11 2026

Authored By Prime Research | Last Modified: Feb 11, 2026 10:36 AM IST

Margin Pressure Visible; Investing in Specialty Assets

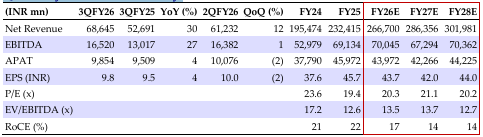

EBITDA grew 36% YoY, led by a 30% YoY sales increase (M&A-led) as muted US sales (flat QoQ) were offset by 13% YoY growth in India and contributions from M&As (Amplitude, Comfort Click). While gross margin improved by 330bps YoY (to 73.2%), higher costs from M&As (staff/SG&A up 20%/58% YoY) resulted in a muted EBITDA margin of 24.1% (down 64 bps YoY). The company expects to meet its guidance of single-digit growth and a margin above 26% in FY26 and 23%+ in Q4FY26. For the US business, steady growth is expected in FY27, led by continued traction in gMyrbetriq, new launches (40+ including complex generics and exclusivity launches), ongoing momentum in the base business, and scale-up in its specialty segment (505-(b)(2)). Optimism remains for its specialty business with visibility of (1) steady traction from Sitagliptin 505(b)(2) brands, (2) approval for Zycubo (CUTX101) in the US, (3) Saroglitozar NDA filing in Q4FY26/H1FY27, (4) in-license Beizray, a oncology 505(b)(2) brand; launched in the US in Q4FY26, (5) in-license Nufymco (bRanibizumab) and hopes to enter the US market in H2FY27, (6) FYB206 (bKeytruda) phase-1 read-out is expected in H1CY26; launch visibility in CY28, and (7) Usnoflast under development. Patent litigation is ongoing for Mirabegron, no comments on settlement. It guides for an SG&A (ex-R&D) run-rate of INR 16-17bn; incremental costs related to commercial and pre-launch activities for its specialty products to increase SG&A/ employee costs (new hirings), and R&D to remain at 7.5-8% of sales. Factoring in Q3 and margin outlook, we have cut EPS by 2/3% for FY26/27E and revise TP to INR 1,000 (23x Q3FY28E). ADD stays, as the broader thesis of steady growth in the US and India, monetization of R&D assets, Medtech scale-up intact. However, the declining margin to ~26%+ in FY26 and ~23.5% in FY27/28 (from 29.8% in FY25) remains a key concern.

Zydus Lifesciences Q3 Highlights

Sales grew 30% YoY to INR 68.64bn (ex-M&A growth was in low double-digit) as the US sales (41% of sales) at USD 314mn were flat QoQ on negligible gRevlimid sales and +10% YoY, led by traction in gMyrbetriq and new launches. India formulations (25%) grew 13% YoY. Wellness (14%) grew 113% YoY. EMs/EU (12%) grew 38% YoY, API (3%) grew 26% YoY, and Medtech sales was at INR 2.9bn. Higher GM (+330 bps YoY to 73.2%) and higher staff/SG&A (+20/ 58%) led to EBITDA^ of INR 16.5 bn (+27% YoY) and 24.1% margin (-64 bps). Higher interest (+306% YoY), depreciation (+57%), and other income (+94%) led to a PAT^ of INR 9.8bn (+13% YoY).

Con Call Takeaways

Volume quota for gRevlimid exhausted in 9M; no sales in Q4. Semaglutide launch will be in the first wave of launch after patent expiry in India; RoW market entry is expected in FY28. The company completed acquisition of two biologic CDMO plants from Agenus Inc (for USD 90 mn); it expects scale-up over the next 2-3 years.

Zydus Lifesciences Quarterly Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 11 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.