HSIE Institutional Report: Bharat Forge Feb, 13 2026

Authored By Prime Research | Published at: Feb 13, 2026 01:08 PM IST

Execution of the Defense Orderbook to Pick Up

Order execution for the defense segment sees a meaningful improvement in Q3, with sustainable growth expected for the coming years on the back of superior design and manufacturing capability of the company that allows it to consistently expand the product portfolio. Going forward, we also expect operating leverage as well as better mix to help expand margins in the defense segment. Additionally, with the interim deal between India and the US in place, it provides for a restocking opportunity over the near to medium term, and for customers to resume new product development programs with the company. Considering the long-term business potential of the forging business which is also aided by the China+1 and Europe+1 plays, and of the defense business that would be led by geopolitical tensions, we upgrade our target P/E multiple from 33x earlier to 37x Dec-27 EPS (+2 SD of 4-year mean) for a TP of INR2,031 and maintain a BUY rating.

Consolidated Performance

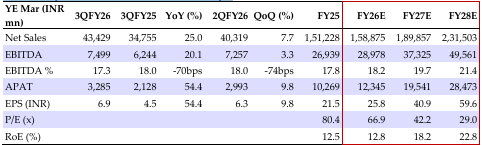

Q3FY26 EBITDA margin came in at 17.3%, down 70bps YoY and 74bps QoQ, below our estimate of 18.5% and Bloomberg consensus estimate of 19%, impacted by the slowdown in the CV exports segment in standalone operations.

Standalone Performance

Q3FY26 EBITDA margin came in at 27.2%, down 191bps YoY and 112bps QoQ, missing both our estimate of 29.2% and Bloomberg consensus estimate of 28.1%, as domestic auto segments, as well as better execution of orders in the defense segment, covered up for the slowdown of CV segment exports to North America as destocking continued.

Call Takeaways

(1) Management mentioned that INR310mn of US tariff related impact was absorbed in Q3 (up 29% QoQ). (2) Of the new orders of INR 23.9bn won in Q3, ~79% were for defense. (3) The defense order book stands at INR111bn, up 18% on a QoQ basis. (4) It expects the defense segment to grow 30-40% in FY27, aided by the commencement of production of the ATAGS (Advanced Towed Artillery Gun System) and CQB carbines. (5) By FY30, it expects the defense segment to form 18-20% of the revenue mix. (6) It expects the profitability of the defense segment to be equivalent to the core business in due course, supported also by a long tail of after-sales (MRO) revenue stream. (7) On the European operations, it indicated that demand was patchy because of the holiday season in Q3, while capacity utilization levels stood at 60-65%. (8) On the US aluminum business, it highlighted that higher tariffs on aluminum imports into the US have been impacting the segment’s profitability. (9) It expects the aerospace segment to grow meaningfully with new capacities coming online and good contribution to profitability. (10) On CV component exports, it indicated that improvement in Class 8 orders in the US should likely lead to steady business ahead.

Bharat Forge Quarterly/Annual Financial Summary

Source: HSIE Research (HSIE Results Daily Report – 13 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.