HSIE Institutional Report: Oil India Feb, 13 2026

Authored By Prime Research | Published at: Feb 13, 2026 03:35 PM IST

Reduced Crude Price Impact Realization

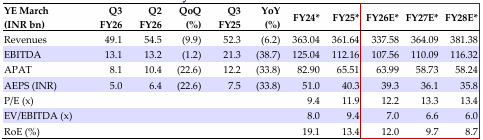

Our BUY recommendation on Oil India with a revised target price of INR 520 is premised on gas production growth at 3% CAGR and oil production growth at 3% CAGR over FY26-28E and tripling of refinery capacity of Numaligarh refinery. Q3FY26 standalone EBITDA at INR 13.08bn (-38.7% YoY, -1.2% QoQ) and PAT at INR 8.08bn (-33.8% YoY, -22.6% QoQ) were below our estimates. The miss was due to lower-than-expected per unit gas sales realization and higher-than-expected opex, partially offset by lower staff cost. Oil and gas production stood at 1.66mmtoe (-2.2%YoY, +0.4% QoQ).

Standalone Financial Performance

EBITDA for Q3FY26 came in at INR 13.08bn (-38.7% YoY, -1.2% QoQ). Other expenses stood at INR 19.04bn (+47.8% YoY, -17.1% QoQ). PAT stood at INR 8.08bn (-33.8% YoY, -22.6% QoQ). Depreciation was at INR 6.40bn (+21.6% YoY, +10.9% QoQ) and interest cost was at INR 2.6bn (+9.1% YoY, +2.4% QoQ).

Oil India Q3FY26 Standalone Operational Performance

Net crude oil realization stood at USD 61.3/bbl (-14.3% YoY, -7.5% QoQ) and gas realization was at USD 6.57/mmbtu (+1.0% YoY, -1.4% QoQ). Oil production came in at 0.858mmt ( 1.2% YoY, +1.2% QoQ). Gas production of 0.801bcm (-3.4% YoY, -0.4% QoQ) was recorded in the quarter. Oil sales volume was at 0.82mmt (-1.1% YoY, 1.3% QoQ), while gas sales volume was at 0.66bcm (-3.2% YoY, +0.2% QoQ).

Conference Call Highlights

(1) NRL – reported gross refining margin of USD 16.2 per barrel for the quarter as against USD 10.56/bbl reported in the previous quarter. The improvement in gross refining margin was due to higher diesel cracks in Q3FY26, which makes up ~ 65% of NRL’s product slate. NRL commissioned the CDU and VDU units of the expanded refining capacity in the month of December 2025. Stabilization of these units is expected by the end of Q4FY26. Management expects this expanded refinery to achieve 50% utilization by the end of FY27, which would add close to 1mmt to the total throughput. Management is optimistic of the expanded capacity achieving 100% utilization by Q2FY28. The petchem plant could commence operation by the end of FY28 and achieve 100% utilization by Q2FY29. (2) OINL – Reduction in crude oil prices resulted in lower per unit realization which impacted revenue growth in the quarter. (3) Management noted that contractual costs increased significantly in the quarter due to increased deeper drilling activity undertaken. OINL aims to achieve 3.8/4MMT of oil production in FY28/29 and 5 BCM of gas production. (4) FY27 capex guidance for standalone entity – INR 92bn with further upswing in FY27.

Change in Estimates and Valuation

We tweak our FY26/27E EPS estimates by -8.4/-2.1% to INR 39.3/36.1, factoring in the reduced oil realization. We value Oil India’s standalone business at INR 234/sh (8x Mar-27E EPS) and its investments at INR 286/sh, leading to a target price of INR 520/sh.

Standalone Financial Summary

Changes in Estimates

Source: HSIE Research (HSIE Results Daily Report – 13 Feb 26 )

Disclaimer

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.