A Surprise From The RBI: India Steps Into A ‘Goldilocks’ Moment

Authored By HDFC SKY | Last Modified: Jan 14, 2026 12:47 PM IST

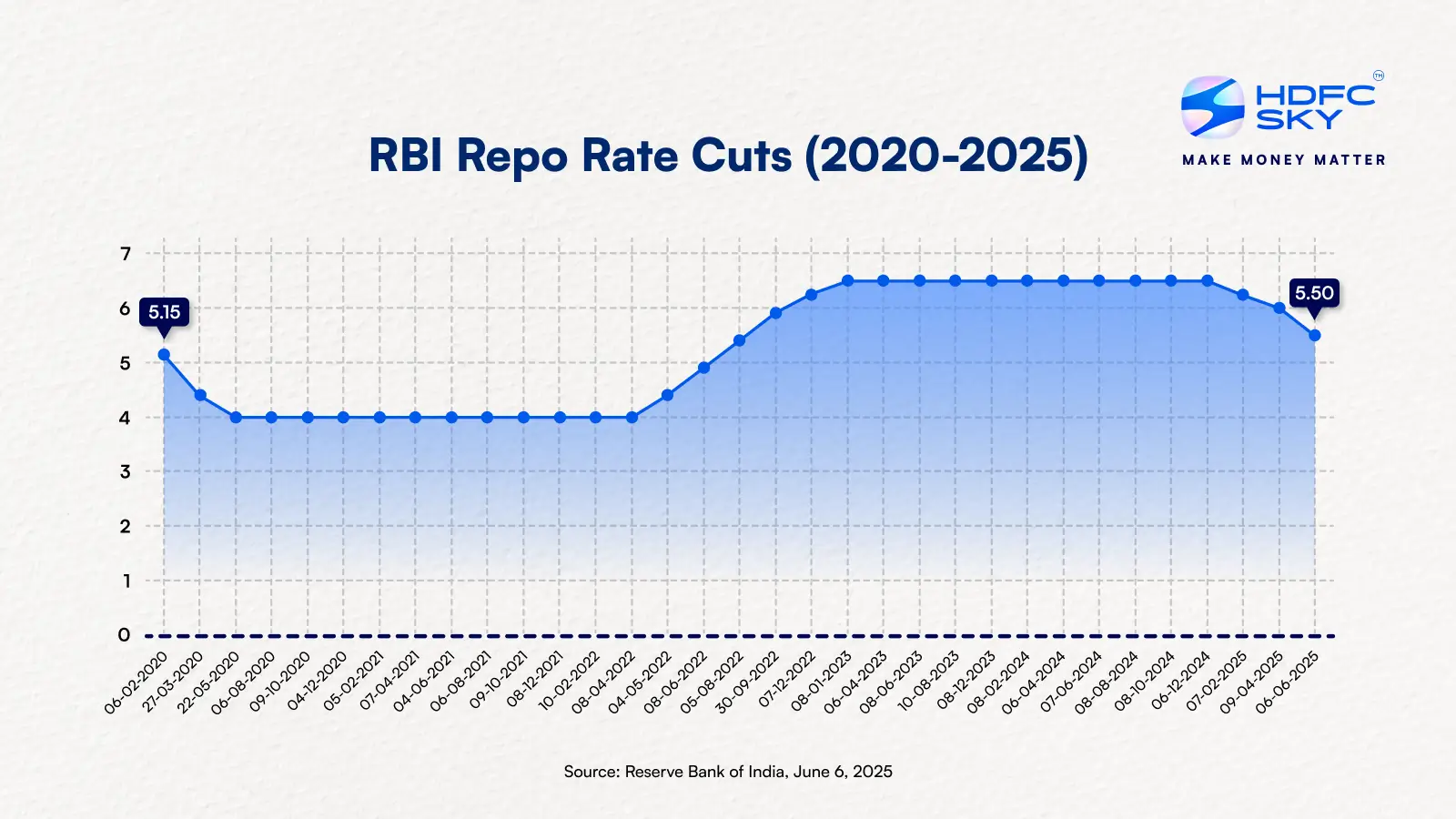

In early June 2025, India’s central bank dropped a major surprise. The Reserve Bank of India (RBI) slashed the benchmark repo rate by 50 basis points to 5.50% and simultaneously announced a phased reduction of the Cash Reserve Ratio (CRR) by 100 basis points, bringing it down to 3%.

By cutting both the repo and CRR in tandem, the central bank has sent a strong signal that it’s ready to inject liquidity and revive demand aggressively.

To understand the significance of this move, it’s worth noting that rate cuts not only reduce borrowing costs for businesses and consumers, but also boost credit flow in the economy.

And when the CRR is reduced, banks have more funds to lend, which can further stimulate demand across sectors like housing, infrastructure, and MSMEs.

This marked the third consecutive rate cut in 2025, bringing the total easing to an aggressive 100 bps since February. RBI Governor Sanjay Malhotra described the move as a “front‑loading” of rate cuts to propel growth while transitioning from an “accommodative” to a “neutral” stance.

This shift is particularly important because it signals that the RBI is now confident inflation is under control, allowing it to pivot focus toward growth.

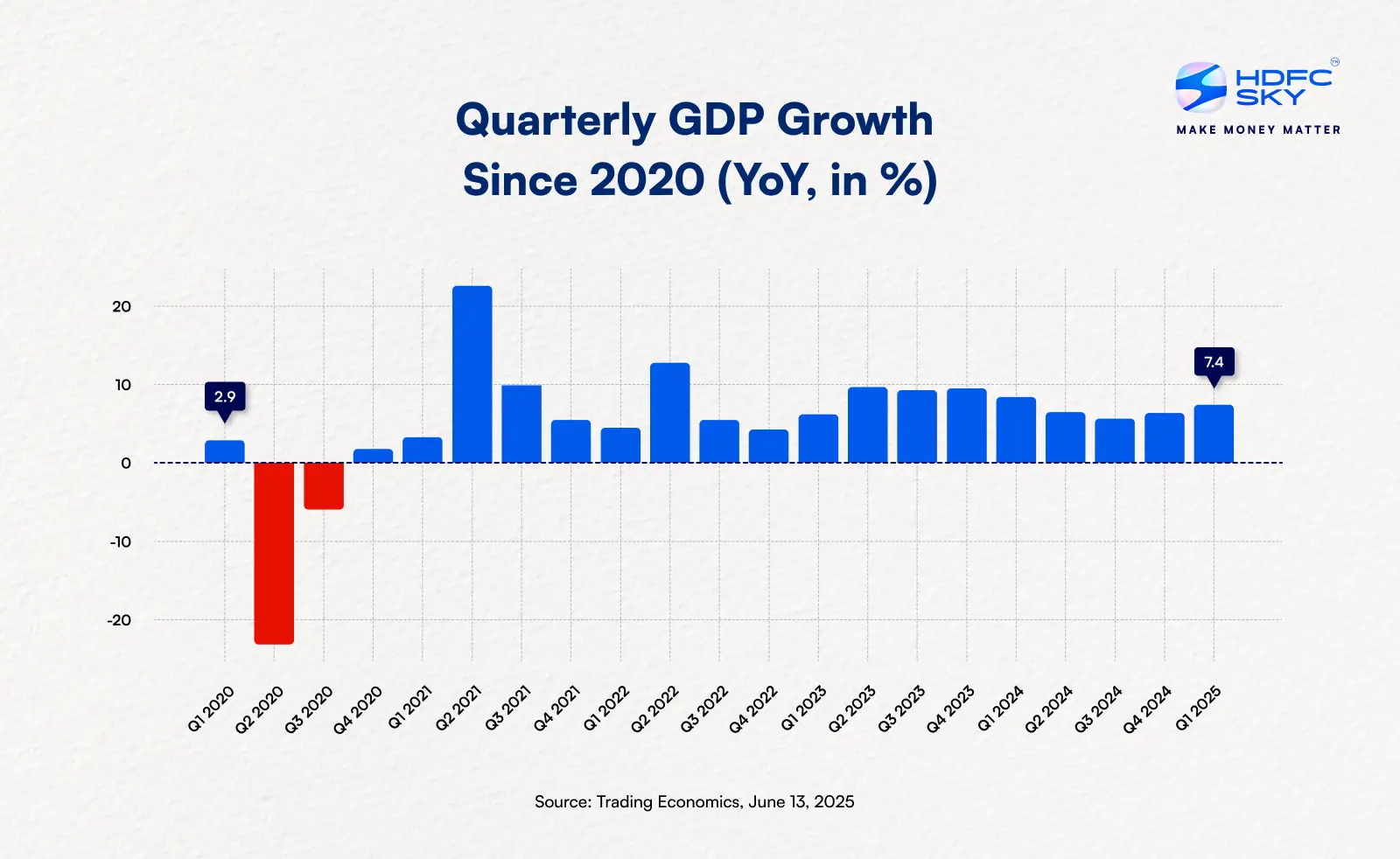

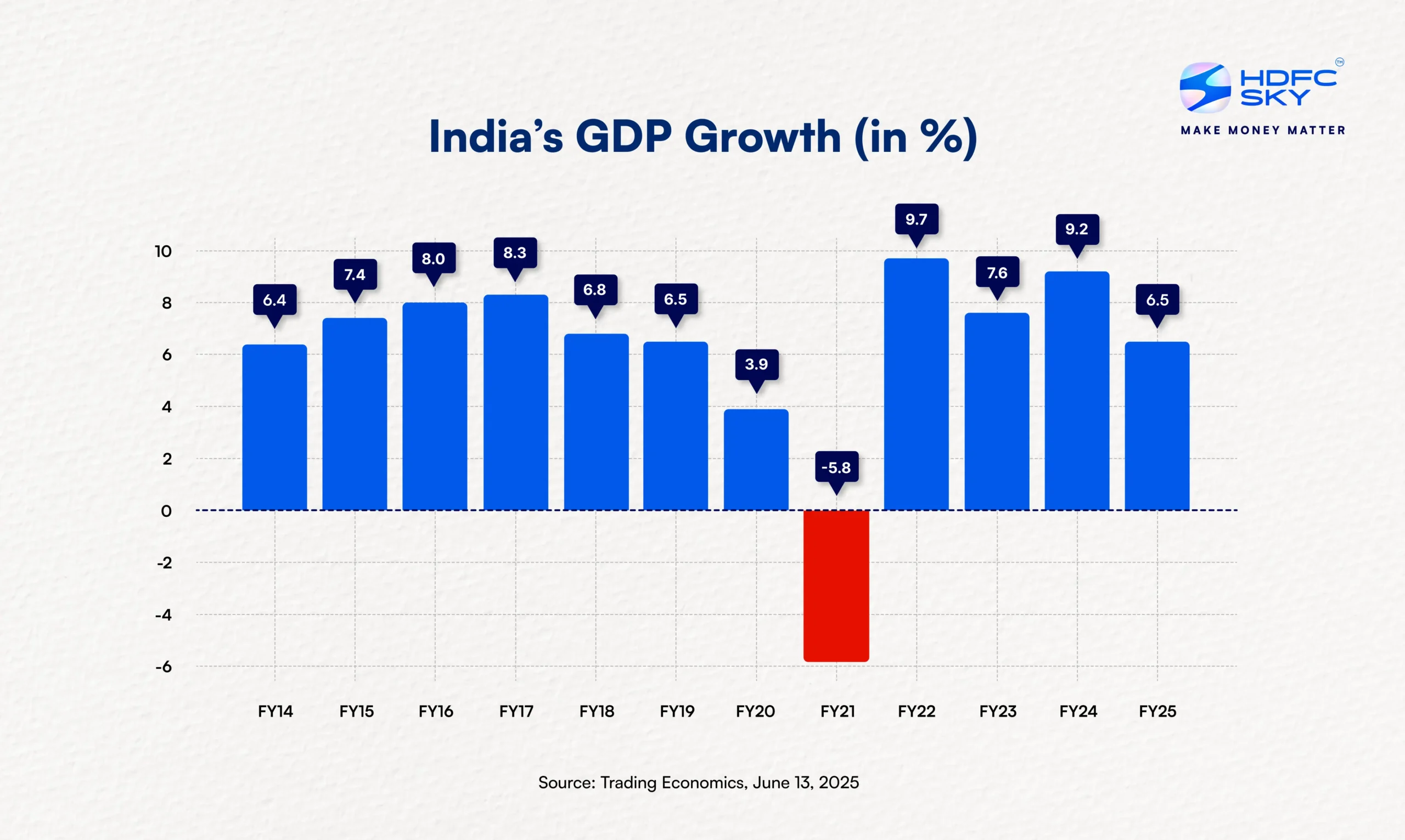

India’s GDP growth surged to 7.4% in the January-March quarter and the central bank projects the economy will expand at 6.5% this financial year.

Rajiv Batra, Head of Asia Equity Strategy at JPMorgan, believes Indian markets are stepping into a “Goldilocks” phase after RBI’s larger-than-anticipated rate cut.With inflation easing, liquidity improving, and borrowing costs declining, he expects this environment to support growth.

Batra anticipates widespread gains across sectors like banking, NBFCs, consumption, and real estate, though he maintains a cautious outlook on IT and auto stocks.

These sectors are typically interest-rate sensitive, meaning they benefit directly when the cost of capital comes down. For instance, NBFCs depend heavily on borrowing from banks and a lower repo rate reduces their funding costs, potentially improving their margins and credit disbursal capacity.

At the same time, analysts are watching how quickly the benefits of this rate cut will transmit into the real economy. The focus now shifts to whether banks will pass on the lower rates to consumers, and how industries respond in the coming months.

While the RBI sets the tone, real impact is felt only if banks reduce EMIs, offer competitive business loans, and spur retail credit growth.

What Is Goldilocks?

The term “Goldilocks” (in economics or markets) refers to a “just right” scenario, where growth is strong enough to avoid recession but not so strong that it triggers inflation.

Economist David Shulman is widely considered to have coined the phrase “Goldilocks economy” in an article published in 1992, “The Goldilocks Economy: Keeping the Bears at Bay.”

The U.S. economy of the middle to the late 1990s was considered a Goldilocks economy because it was “not too hot, not too cold, but just right,” a phrase that has been used to describe the ideal economy for investors.

Understanding A Goldilocks Economy

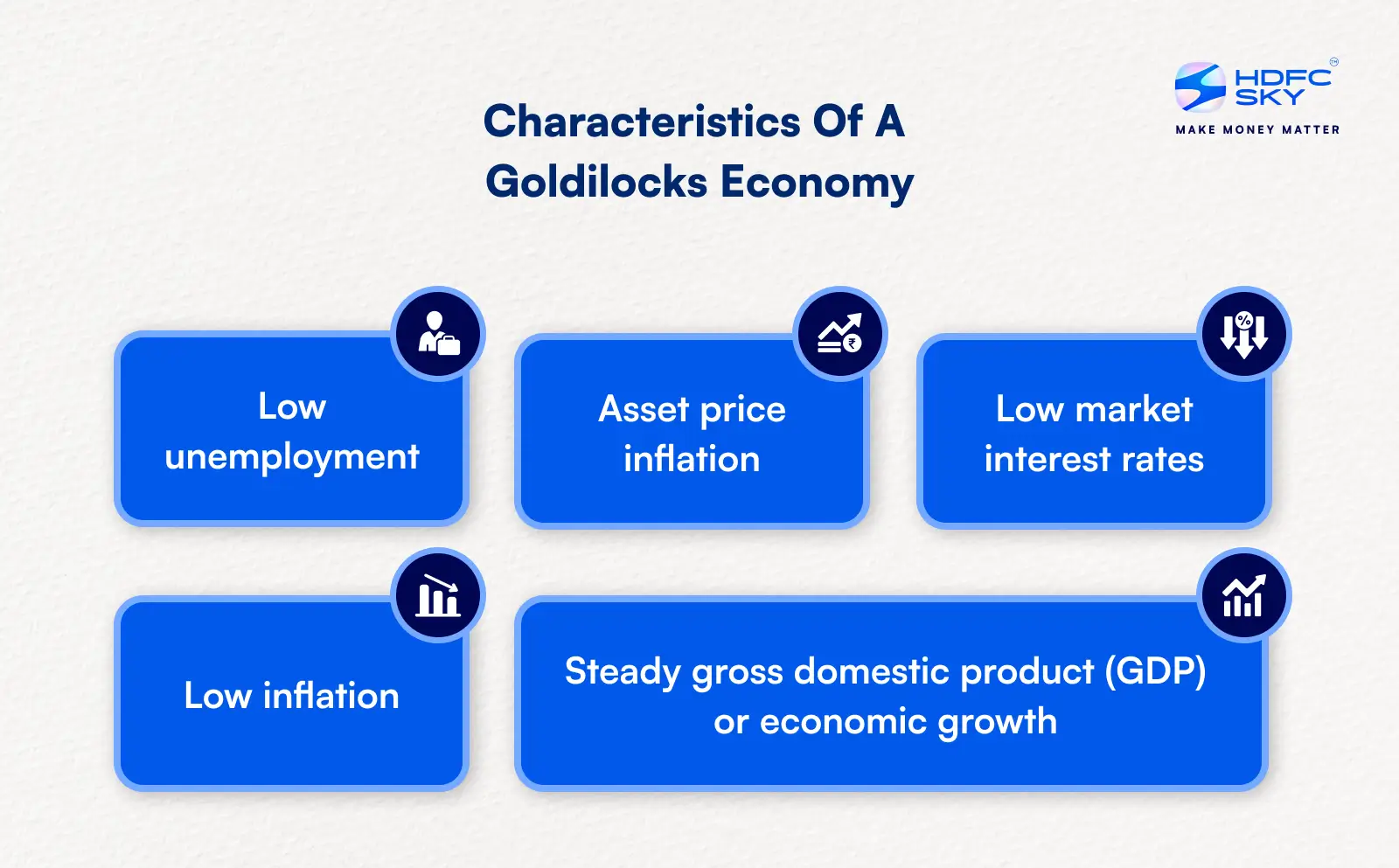

A Goldilocks economy strikes the right balance between growth, employment, and inflation.

The ideal conditions are typically characterized by:

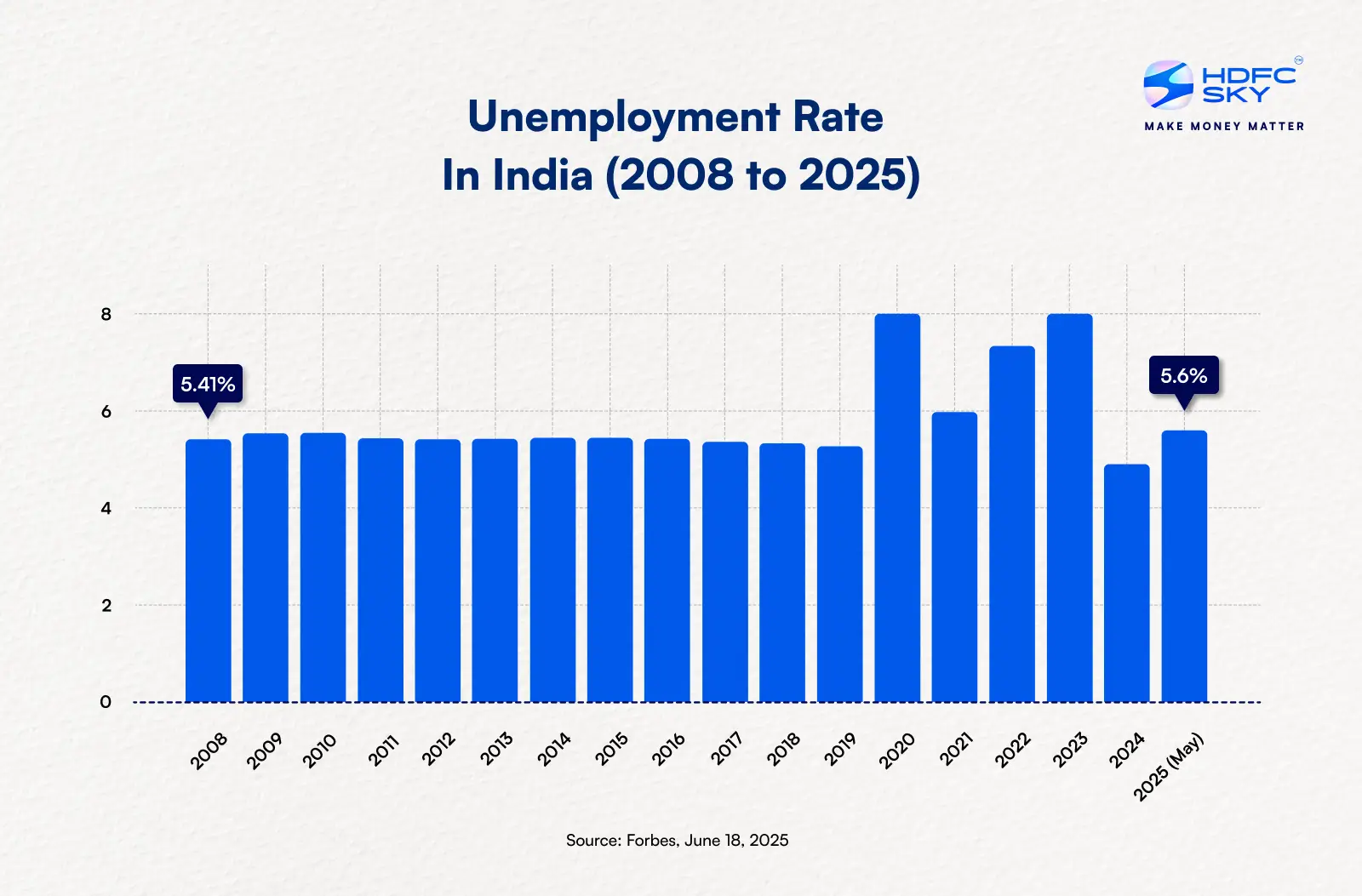

- Low unemployment: In India, the employment rate tells us what portion of working-age Indians are actually working. If the unemployment rate is low, it signals that most people who are willing and able to work are finding jobs.

This typically reflects a healthy labor market, steady economic activity, and rising income levels.

Take a look at the unemployment rate in India for the last 17 years. What’s notable here is that despite periodic volatility, India has managed to keep unemployment under relative control.

- Asset price inflation: An increase in the prices of stocks, derivatives, bonds, real estate, and other assets signals a Goldilocks economy.

- Low market interest rates: These rates are the percentage of a rupee amount that a lender will charge a borrower when they lend money. Low market interest rates refer to the reduced cost of borrowing money, meaning lenders charge less interest on loans.

This often encourages businesses and consumers to borrow and invest more, boosting economic activity. In a broader sense, such interest rate environments also impact investor behavior.

With lower returns on fixed income instruments, investors may seek higher yields through equities or real estate, further stimulating economic activity.

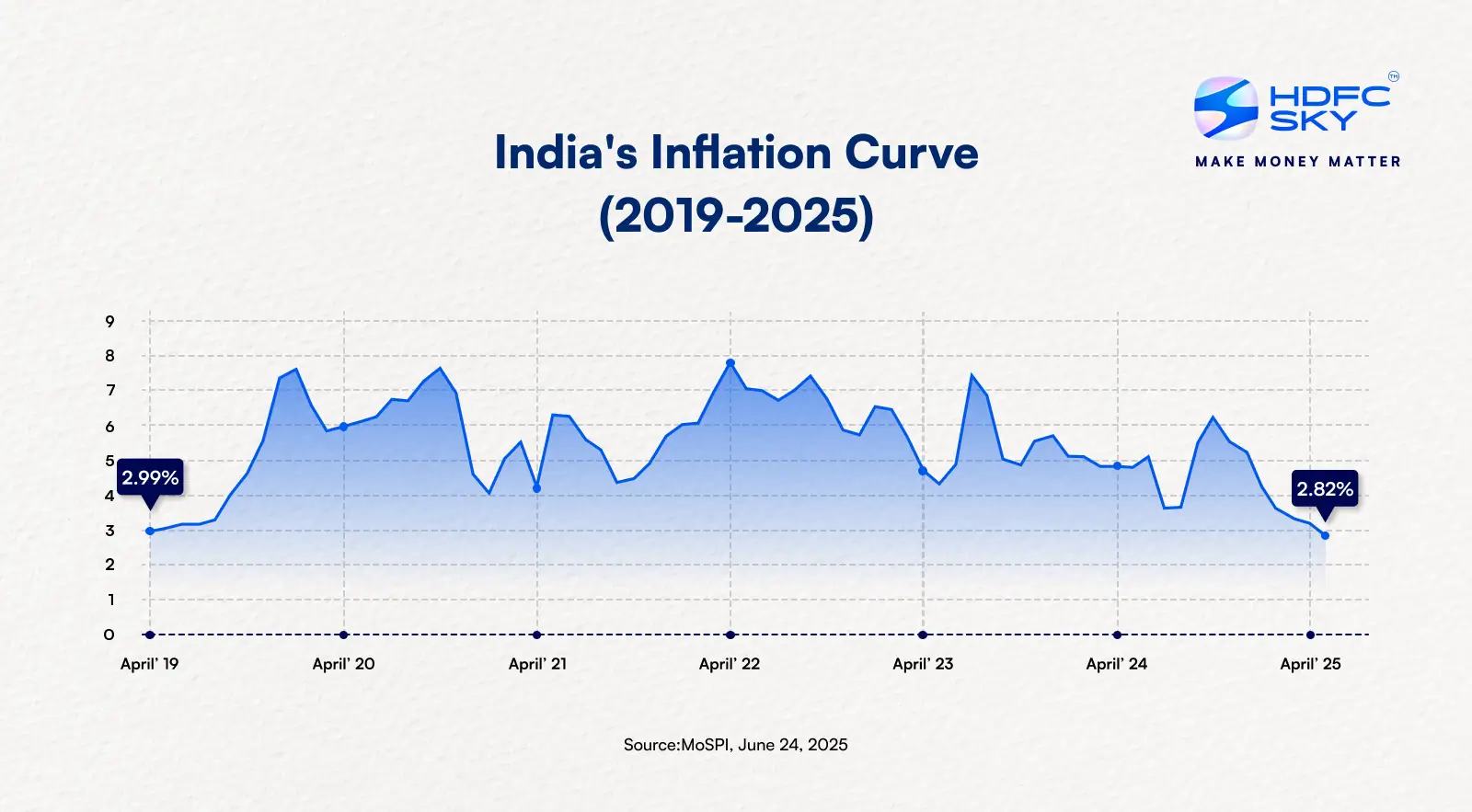

- Low inflation: This is tracked using numbers like the Consumer Price Index (CPI), which measures how much prices are rising for everyday items. Inflation describes the purchasing power of a nation’s money.

And now, the inflation has fallen to 2.82% in May 2025, the lowest in the last six years.

- Steady gross domestic product (GDP) or economic growth: This is the most cited indicator of a Goldilocks economy. GDP is a broad economic measure of the value of all services and finished goods that are produced in a country and it’s a direct indicator of the health of an economy.

A consistent trend of 6-8% GDP growth, even amid global turbulence like COVID-19 or geopolitical uncertainties, has positioned India as one of the few large economies with resilient fundamentals.

This resilience is what underpins the current optimism about a Goldilocks phase.

For a Goldilocks phase to be sustainable, macroeconomic indicators must stay in balance over time. This means inflation should remain low but positive, job creation should be steady, and credit growth must support productive sectors.

Goldilocks And The Central Bank

In India, RBI manages the money supply and banking sector through monetary policy tools like repo rates. Its goal is to maintain a Goldilocks economy where growth is steady and inflation remains in check.

When growth slows, the RBI may cut rates to encourage spending and investment. But if inflation rises too quickly, it can hike rates to cool demand. Striking the right balance is crucial.

This is where central bank credibility comes in. Markets, businesses, and consumers must trust that RBI will act swiftly and wisely. Any miscalculation could lead to overheating or stagnation, derailing the delicate balance.

Global factors also play a role. Decisions by other central banks, like the US Federal Reserve can influence capital flows and inflation in India, affecting RBI’s policy choices.

In recent months, RBI has walked a tightrope that is trying to revive growth without triggering inflation. With global uncertainties like oil price fluctuations and geopolitical tensions, the RBI’s job becomes even more complex.

Yet, the current environment gives policymakers a rare window to steer the economy toward stability. And perhaps, more than stability, it presents a moment to structurally reposition India’s economy.

With global supply chains shifting and capital looking for stable emerging markets, India’s current macro stability offers an opening to attract long-term investments.

The Bottom Line

It can be challenging for central bankers and governments to engineer a Goldilocks economy because many factors must come together for this economic state to exist. The unemployment rate, inflation rate, market interest rates, and gross domestic product (GDP) must all be in ideal, healthy condition. It can’t just be a flash in the pan but should be a steady economic environment. A Goldilocks economy can provide an ideal time for investing but be cautious and keep an eye on the contributing data.