RBI Cuts Rates: What It Means For The Indian Economy

Authored By HDFC SKY | Published at: Jun 9, 2025 06:10 PM IST

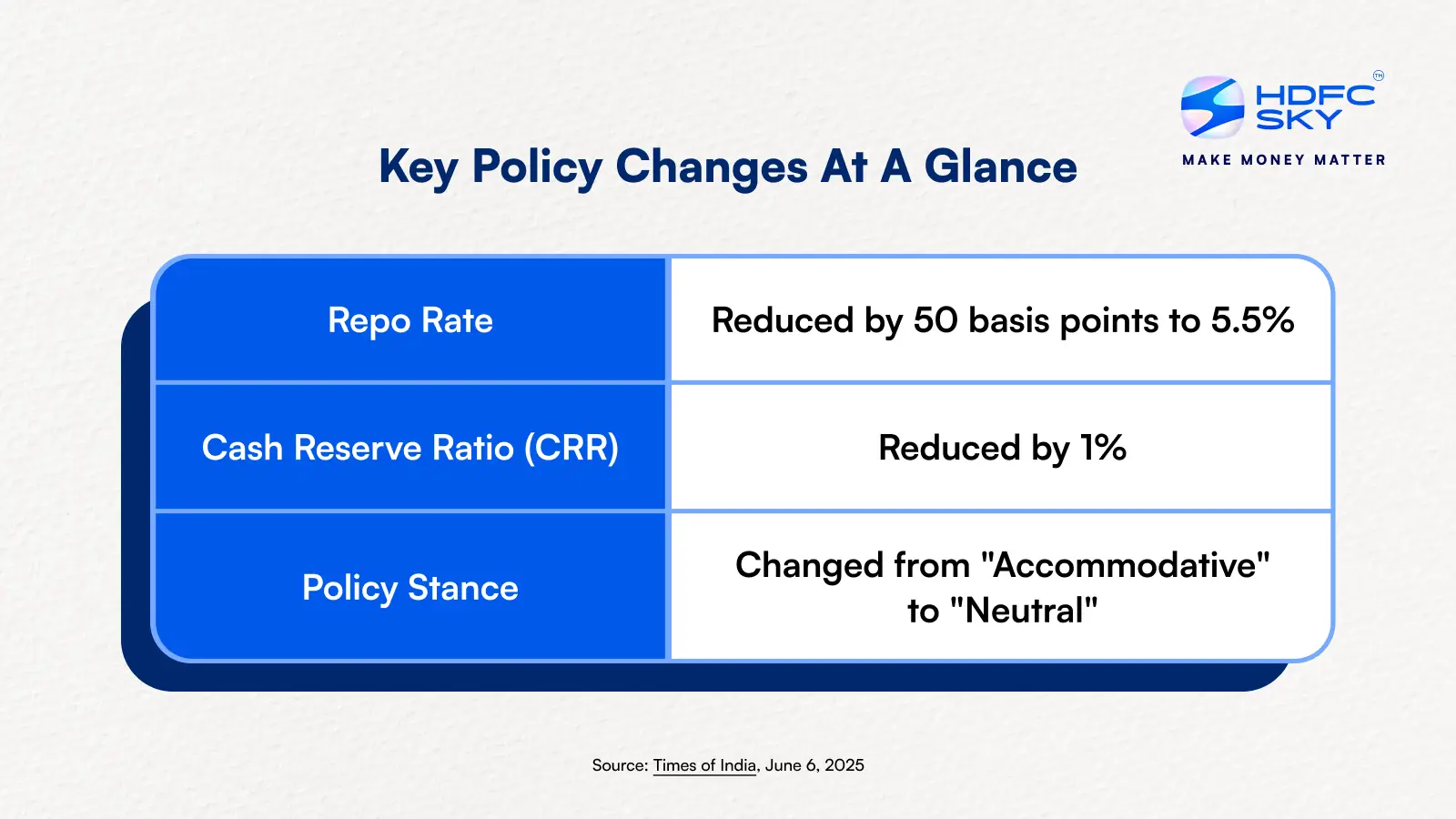

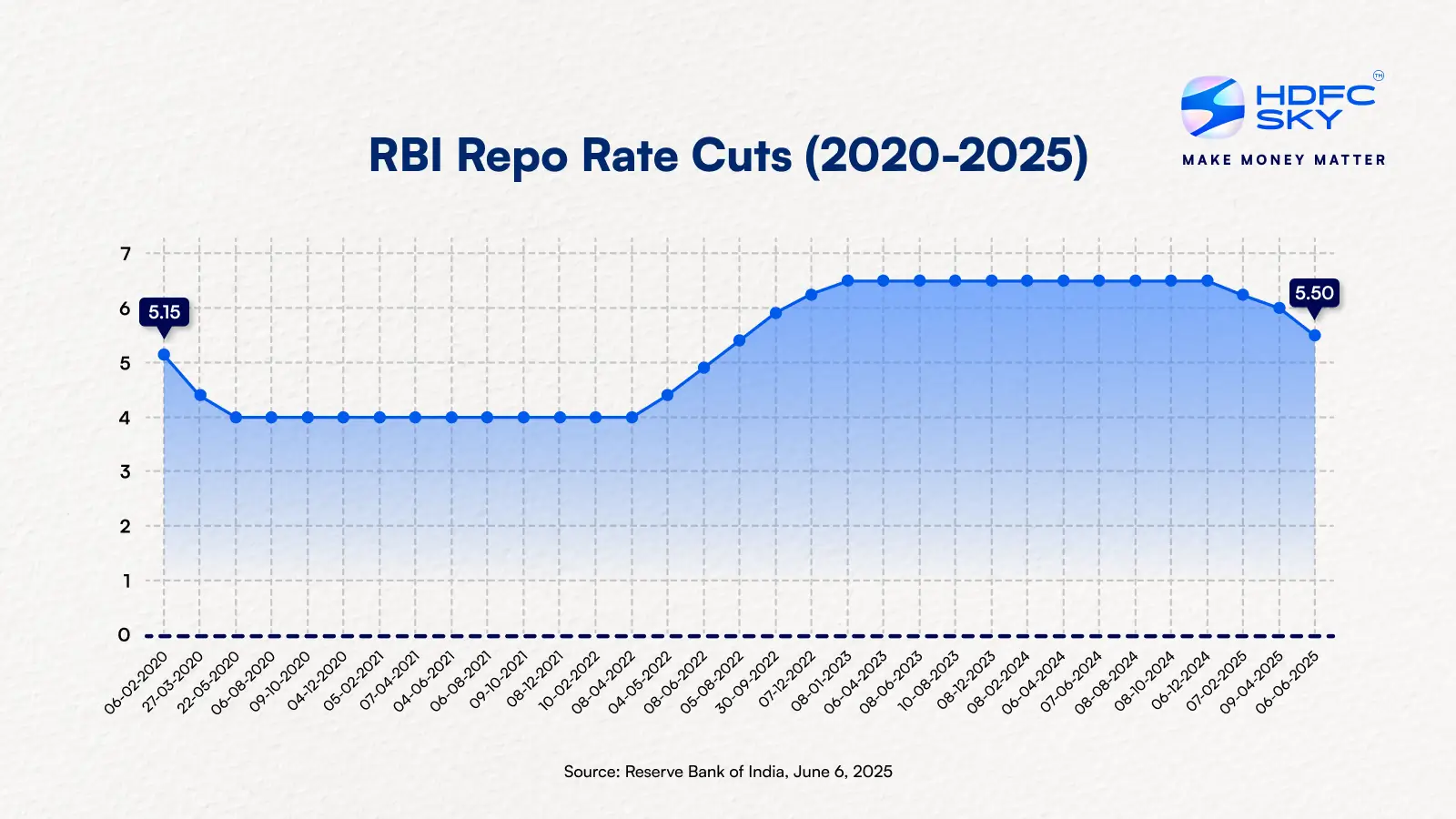

On June 6, 2025, the Reserve Bank of India (RBI) surprised markets with an aggressive monetary policy move. They slashed the repo rate by 50 basis points, bringing it down to 5.50%.

They also announced a staggered 100 basis points reduction in Cash Reserve Ratio (CRR) to 3%, which will inject about ₹2.5 lakh crore into the banking system.

This move was bigger than what most analysts expected.

Let’s understand why the RBI did this and what it means for people, businesses, and the overall economy.

Why Did The RBI Cut The Rates?

The RBI’s monetary policy decisions hinge on two critical factors:

- Inflation Control: How fast prices are rising.

- Economic Growth: How fast the economy is expanding.

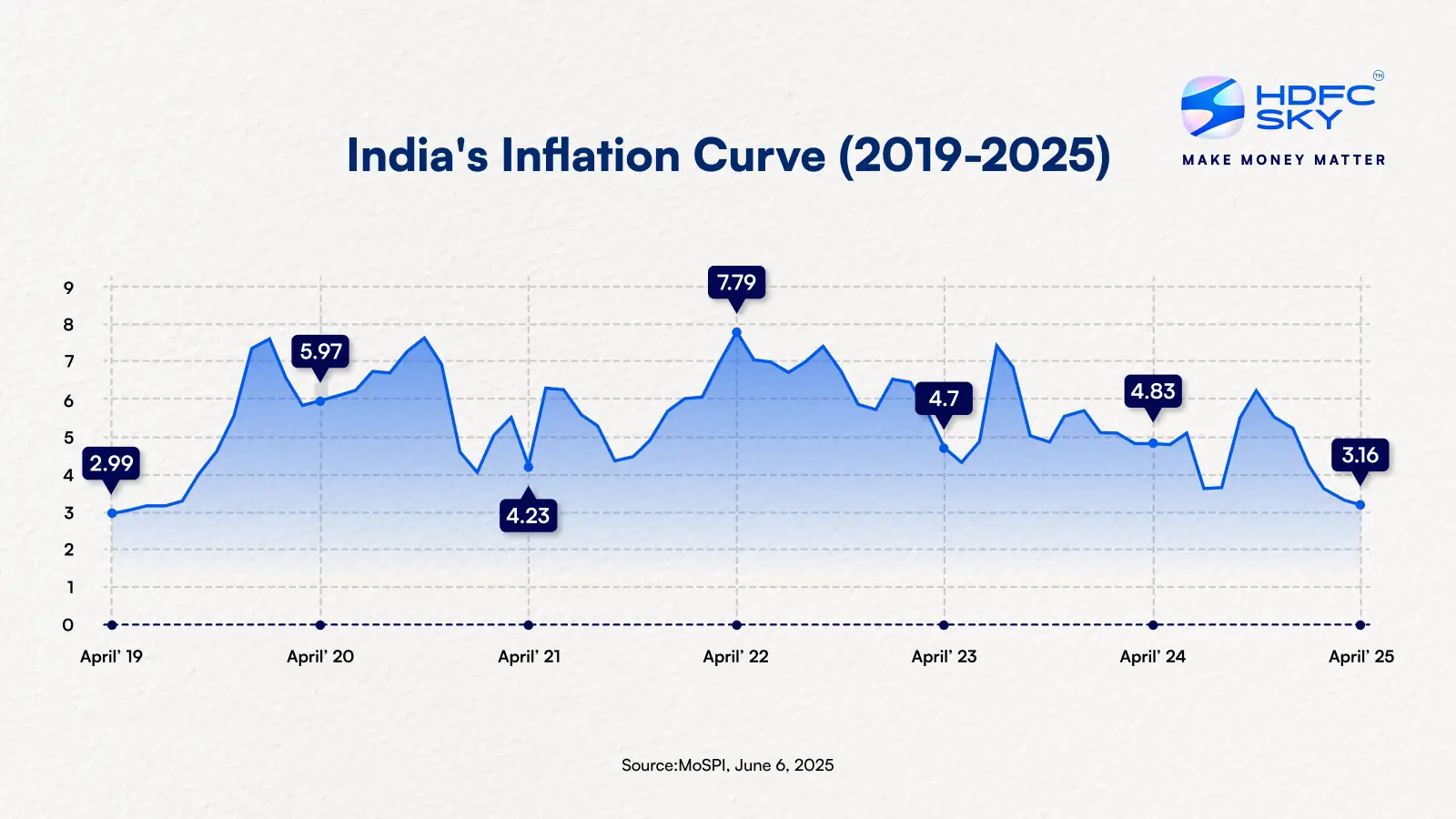

In the past few months, inflation has been under control and prices of essential goods haven’t risen much. Inflation rate in April 2025 was around 3.16%, which was a 6-year low and well within the RBI’s comfort zone.

This gave RBI the confidence to act. With inflation well-anchored, the central bank had room to prioritise growth over price stability.

Meanwhile, on the growth front, things are more delicate. RBI Governor Sanjay Malhotra pegged real GDP growth at 6.5% for FY 2025–26. But there are signs of cooling momentum, especially due to external headwinds like U.S. trade policy shifts and geopolitical uncertainty.

The most concerning trend is a notable decline in credit growth. As of mid-May 2025, credit growth plummeted to 9.8%, from 19.5% a year ago. More alarmingly, lending actually shrank in April and May, while deposits rose. That’s not a good sign for an economy that needs steady lending to grow.

By cutting rates, the RBI is trying to reignite lending and consumption, making credit cheaper and encouraging both businesses and individuals to borrow and spend

Understanding The Mechanics: How Rate Cuts Works

The Repo Rate Effect:

The repo rate is the interest rate at which RBI lends money to banks. When the RBI cuts this rate, banks can borrow money at a lower cost.

This often leads to banks reducing the interest they charge on loans such as home loans, car loans, and business loans.

It also means banks may offer lower interest on savings and fixed deposits.

In short:

- Borrowing becomes cheaper

- EMIs may reduce

- But returns on savings may fall

The CRR Effect:

The CRR reduction is equally significant. CRR is the mandatory share of deposits that banks must keep with the RBI. By cutting CRR by 1%, the RBI l has freed up substantial funds that banks can now deploy for lending.

This liquidity injection of approximately ₹2.5 lakh crore represents a powerful tool to stimulate the economy.

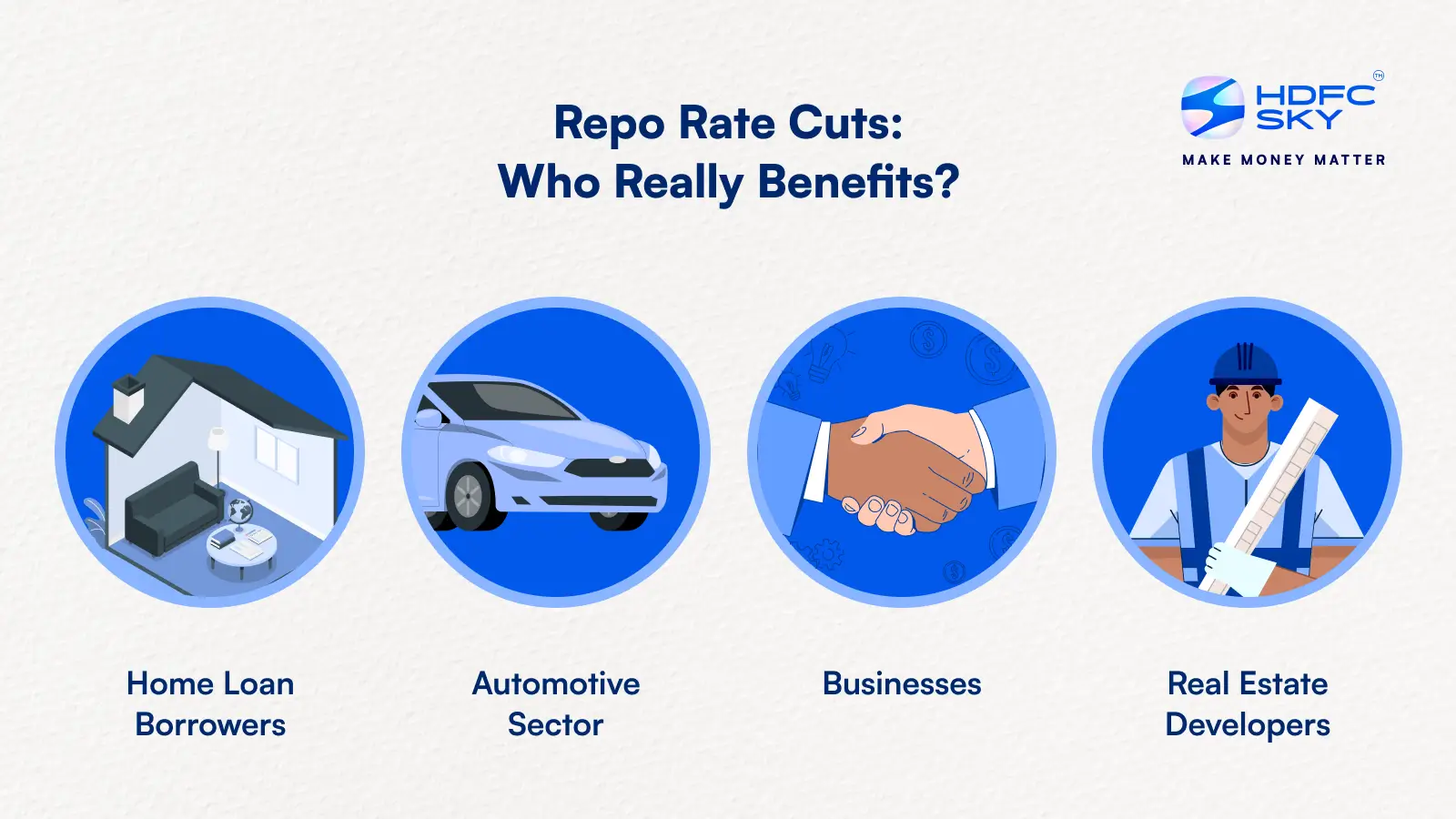

Who Stands To Benefit From This Move?

- Home Loan Borrowers: The rate cut provides substantial relief to home loan borrowers.

Consider this example: A borrower has an outstanding loan of ₹50 lakh at an 8.5% interest rate and a 20-year tenure. With a 100 bps rate cut so far, she could save ₹7.47 lakh over 20 years. Her monthly EMI would reduce from ₹43,391 to ₹40,281, providing immediate cash flow relief.

- Automotive Sector: The automobile industry, which has been grappling with sluggish demand, stands to benefit significantly. Lower financing costs could revive consumer interest in vehicle purchases, potentially boosting sales across segments.

- Businesses: Businesses requiring working capital or expansion funding will find borrowing more attractive. This could translate into increased investment, capacity expansion, and potentially higher employment generation.

- Real Estate Developers: The capital-intensive real estate sector will benefit as lower borrowing costs improve project economics for developers who typically finance 60-70% of costs through debt, enabling them to complete projects faster.

Potential Risks And Challenges

While the RBI’s recent rate cut is aimed at boosting growth and reviving credit flow, it doesn’t come without trade-offs. There are a few challenges and potential pitfalls to watch out for:

- Slow Transmission

The effectiveness of monetary policy depends heavily on how quickly banks pass on rate cuts to borrowers. While repo rate-linked loans will see immediate benefits, loans tied to the Marginal Cost of Funds based Lending Rate (MCLR) or internal benchmarks may experience delayed transmission.

- Impact On Savers

Fixed deposit holders and conservative investors face the prospect of lower returns. This could particularly affect senior citizens and others who rely on interest income for their livelihood.

- Inflation Can Bounce Back

With ₹2.5 lakh crore of extra money flowing into the economy, there’s a risk that too much demand could push prices up if businesses can’t produce enough goods and services to meet it.

To make things trickier, global dynamics are adding another layer of uncertainty.

Global Factors At Play: Pressure On The Rupee

Emerging markets like India are sensitive to U.S. interest rates because they directly influence global capital costs and the risk appetite of foreign investors.

At present, the U.S. is offering a nominal return of around 5%, along with approximately 2% real growth and 2–3% inflation. This combination makes U.S. assets relatively attractive.

If India lowers its interest rates too much, there is a risk that foreign investors might withdraw funds in search of better returns in the U.S. Such outflows could weaken the rupee and increase the cost of imports.

Adding to the concern are rising oil prices. Since India imports about 88% of its crude oil, any increase in global prices significantly impacts the domestic economy. With Brent crude currently hovering around $65 a barrel, elevated fuel costs could contribute to higher inflation and a wider trade deficit.

Therefore, while the RBI aims to support growth, it must tread carefully. Global factors such as the high U.S. rates and rising commodity prices could limit the extent to which India can pursue further rate cuts.

Final Thoughts

The RBI has shifted from “accommodative” to “neutral,” signaling it will now adopt a wait-and-watch approach based on how economic data and global developments unfold.

In other words, the RBI is easing now, but remains cautious. The priority is to support growth without triggering inflation or financial instability. This was a bold step by the RBI, and it clearly shows they are trying to give the economy a real push.

For consumers, this means EMIs are likely to decrease, making homes and cars more affordable, though savings will earn lower returns. Businesses will find borrowing cheaper, potentially spurring expansion and job creation.

For the overall economy, this move could help boost growth. But it’s not all smooth sailing. The RBI will need to keep monitoring inflation closely, while global factors like oil prices and US interest rate movements could still pose risks.

Disclaimer: At HDFC SKY, we take utmost care and due diligence in curating and presenting news and market-related content. However, inadvertent errors or omissions may occasionally occur.

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please note that the information shared is intended solely for informational purposes and does not make any investment recommendations