UPI: India’s Digital Payment System Goes Global

Authored By Shishta Dutta | Published at: Oct 16, 2025 11:44 AM IST

India’s digital transformation has many milestones, but few match the impact of the Unified Payments Interface (UPI). Introduced in 2016 by the National Payments Corporation of India (NPCI) , UPI has gone from being a local innovation to a global reference point in digital finance.

Today, UPI is not just powering payments within India but is also being adopted and recognized across borders. International institutions such as the International Monetary Fund (IMF ) are now studying UPI as a model for financial inclusion and digital innovation.

To understand its impact, it helps to first see what makes UPI different from earlier payment systems.

What is UPI and Why is it Unique?

At its core, UPI is a real-time digital payment system that allows money to be transferred instantly between bank accounts through mobile apps. But what makes UPI stand out is its interoperability .

Any bank can connect to UPI : Users can choose any app, Google Pay, PhonePe, Paytm, BHIM, or others, and still send money directly to another person’s bank account. No preloading of money into wallets is needed. Payments are instant, secure, and available 24×7 .

Unlike closed systems where users are locked into a single network, UPI was designed as open digital public infrastructure. This openness brings two key advantages : users can choose the app they trust, and providers compete to offer better features and security.

The result is rapid growth, wider adoption, and UPI becoming an everyday part of life for millions.

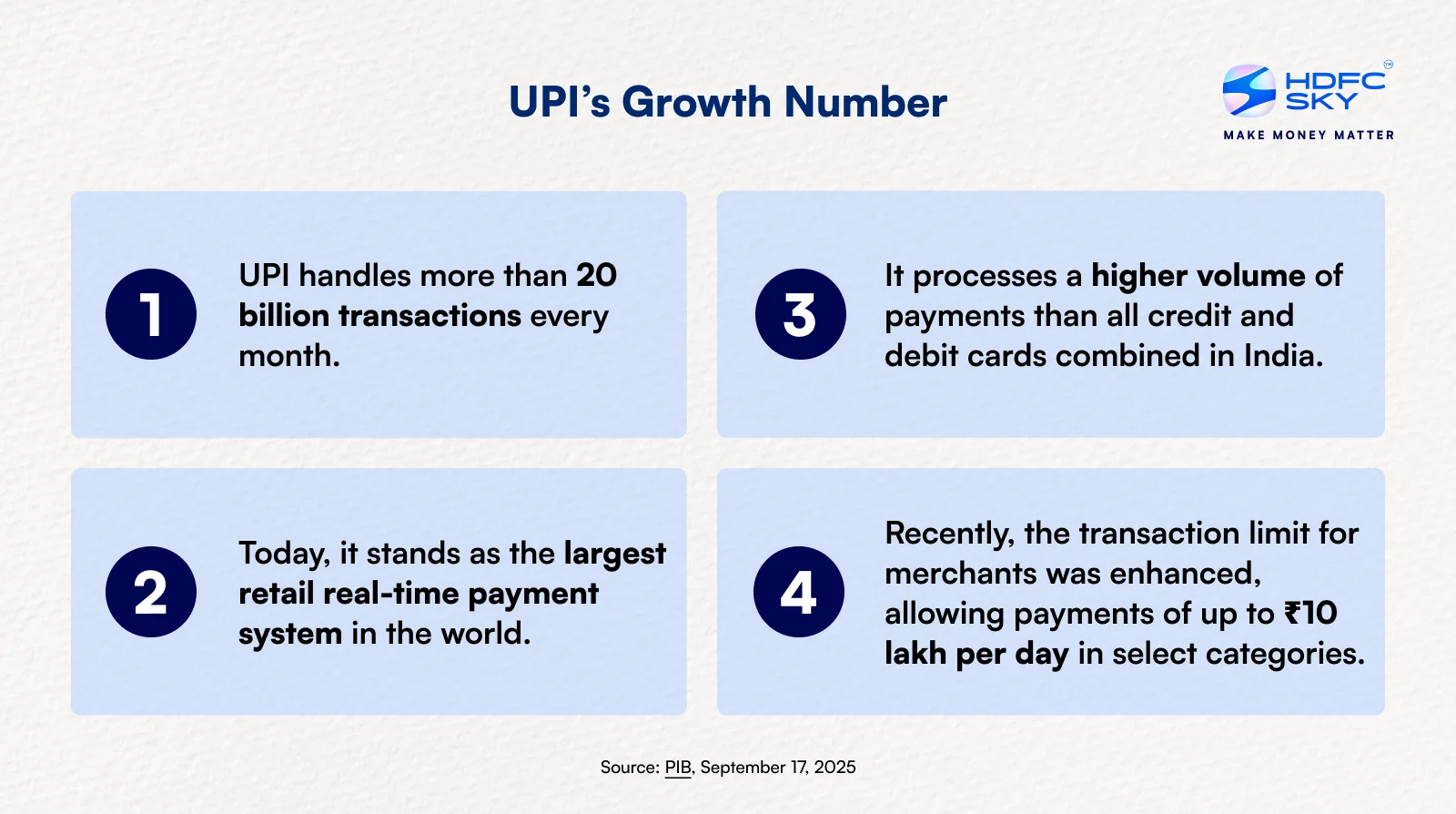

The Scale of UPI’s Growth

UPI’s growth numbers are staggering:

Currently, UPI accounts for 85% of India’s digital transactions and powers nearly half of all real-time payments worldwide.

These figures reflect trust, convenience, and reliability. Month after month, more people and businesses choose UPI, a strong signal that India is steadily progressing toward a cashless, digital-first economy.

From small shops in towns to large e-commerce platforms, UPI is now the default mode of payment for millions of Indians.

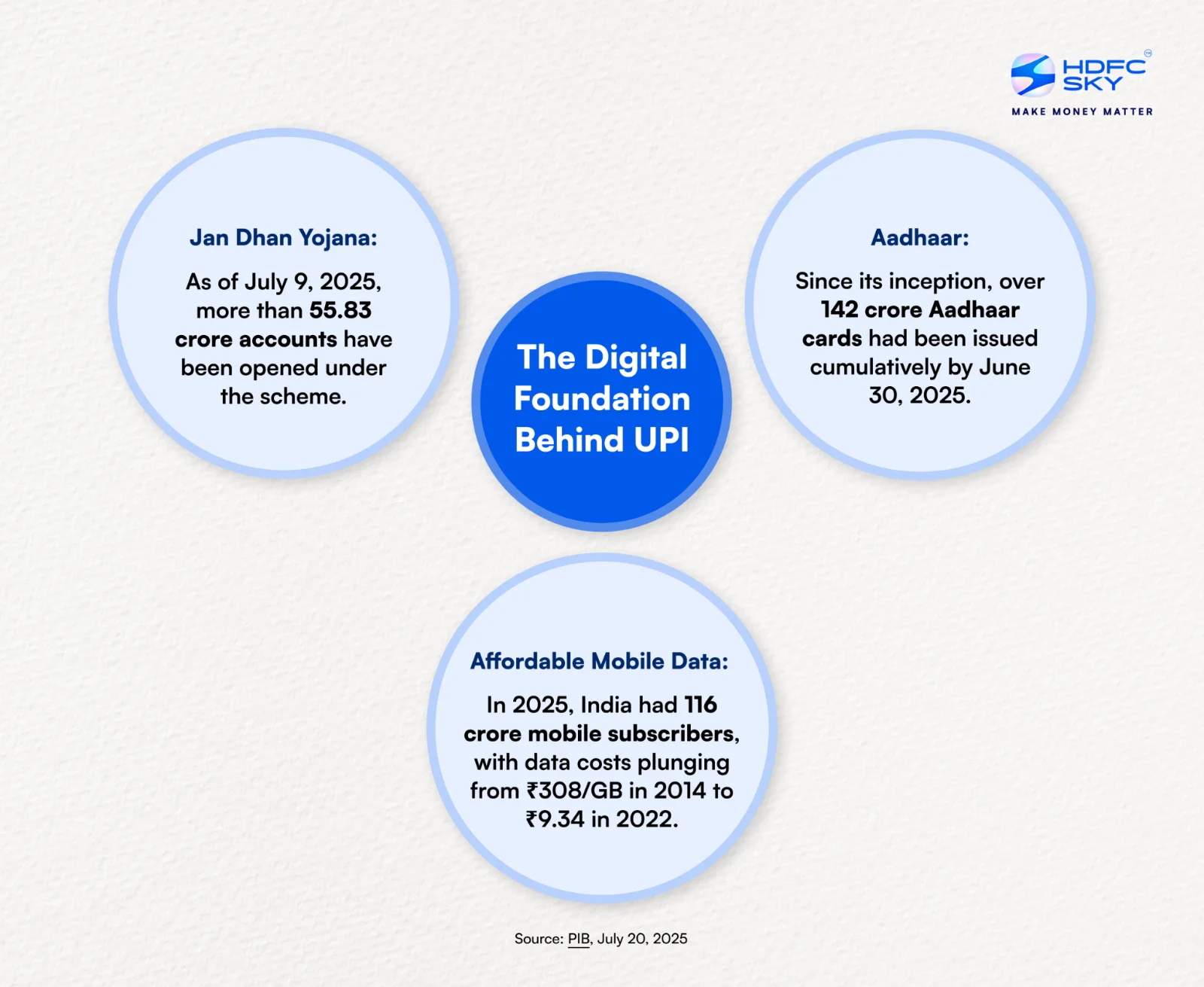

The Foundation: India’s Digital Public Infrastructure

UPI’s success did not happen in isolation. It was built on three important reforms that created the foundation for Digital Public Infrastructure (DPI) in India:

When NPCI launched UPI in 2016, it was able to plug directly into this infrastructure. The result was a payment system that was not just digital but also inclusive and scalable.

India’s dominance in real-time payments is no coincidence. It is the outcome of years of deliberate digital groundwork and a clear vision of using technology to drive inclusive growth. UPI stands as a global benchmark for public digital innovation.

Why Global Institutions are Taking Note

The IMF’s recognition of UPI is a strong validation of its design. In its 2025 Note , the IMF highlighted that UPI has “transformed India’s payment landscape and become the largest real-time payment system in the world by volume.”

The IMF also stressed two key lessons from UPI:

- Interoperability matters: Open systems avoid monopolies and encourage user trust.

- Public-private balance: Government-built infrastructure enabled private players (banks, fintechs, big tech companies) to innovate on top.

This layered and inclusive model is now being studied as a blueprint for other developing nations.

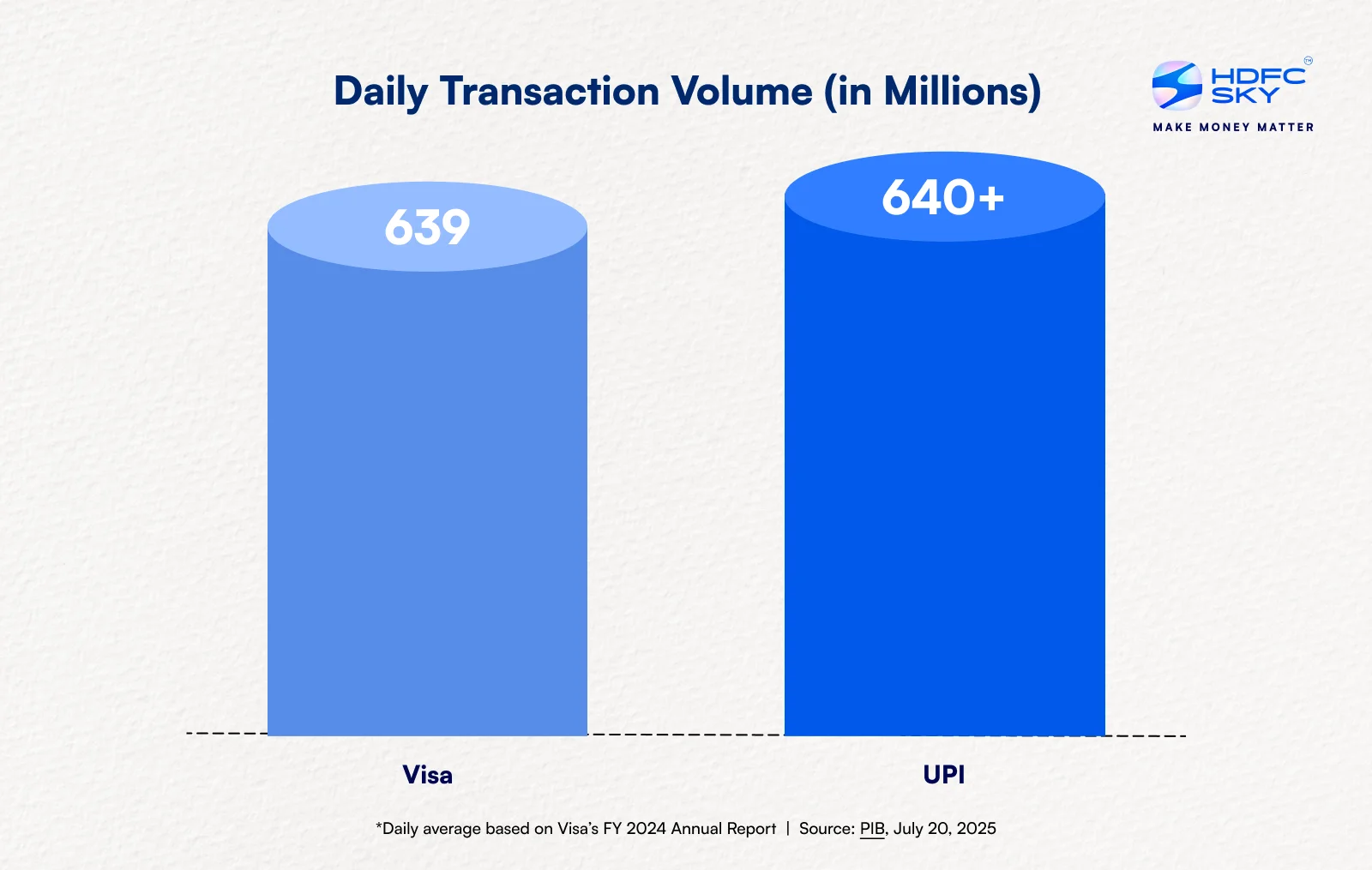

And the numbers tell the story even more powerfully. It is a commendable achievement that UPI processes over 640 million transactions every day, edging past Visa’s 639 million. What makes this achievement remarkable is the speed of its rise – UPI reached this scale in just nine years .

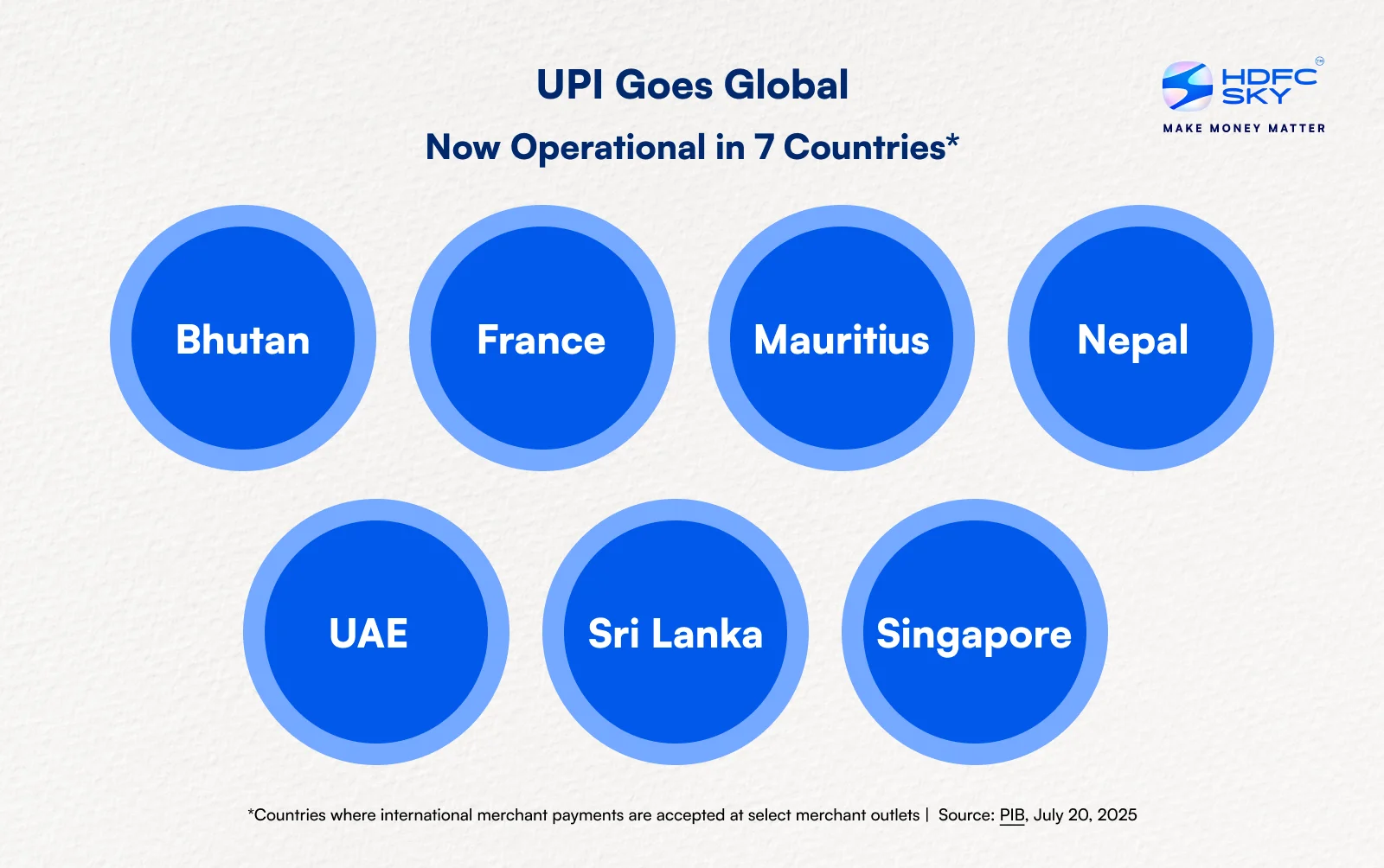

UPI’s Global Expansion

What started as an Indian innovation is now crossing borders through partnerships driven by NPCI International Payments Limited (NIPL ).

In Singapore, UPI is linked with PayNow to power instant cross-border transfers. In the UAE and Mauritius, Indian travellers can make payments for goods and services using UPI. In France, tourists from India can simply scan a QR code at the Eiffel Tower and pay in rupees. Nepal and Bhutan have already adopted UPI for transfers, and discussions are underway with central banks and fintechs across Asia, Africa, and Europe.

This marks a quiet but profound shift. For decades, global finance was shaped by Western institutions and card networks. Today, an Indian-built digital public platform is emerging as an export. UPI is not just moving money across borders, it is carrying India’s reputation for innovation, inclusion, and scale.

Benefits Beyond Payments

UPI is not just about convenience. Its wider benefits include:

- Financial Inclusion: Even small traders and rural households can participate in the digital economy.

- Transparency: Direct digital transfers reduce cash dependency and leakages in government payments.

- Innovation: Open infrastructure allows fintech companies to design new services like credit, insurance, and investments on UPI rails.

The new higher transaction limits also open up UPI for high-value merchant payments, including education, healthcare, and business transactions, further expanding its role in the economy.

Conclusion

UPI’s story reflects India’s larger digital transformation. From being a country heavily dependent on cash, India has now built the world’s largest real-time payment system, which is not only empowering its citizens but also inspiring other nations.

The IMF’s recognition, global partnerships, and rising transaction volumes confirm that UPI is more than a domestic success. It is becoming a symbol of India’s innovation, inclusivity, and leadership in the digital age.

From bank transfers in Indian towns to cross-border payments in global capitals, UPI is proving that a homegrown solution can scale worldwide.

Disclaimer: At HDFC SKY, we take utmost care and due diligence in curating and presenting news and market-related content. However, inadvertent errors or omissions may occasionally occur.

If you have any concerns, questions, or wish to point out any discrepancies in our content, please feel free to write to us at content@hdfcsec.com.

Please note that the information shared is intended solely for informational purposes and does not make any investment recommendations